Weekly Stock Bullfinder- Week of 1/10

Weekly Stock Bullfinder- Week of 1/10

Stocks I'm Watching - Week of 1/10

Happy New Year and I hope everyone had a nice weekend!

Taking a Step Back- What is the Market Telling Us?

In the beginning of the year, it’s a good time to reflect of where things currently stand and what the charts have been telling us over the past few months. Since the “Powell Pivot” in early December, there has been a dramatic shift in the sectors and industry groups where money is flowing into. The “Powell Pivot” refers to Fed Chair Jay Powell’s remarks to Congress in which the notion of “transitory” inflation was officially retired and a more hawkish pivot to prioritizing fighting high inflation was moved up as higher immediate priority. With Friday’s unemployment report moving the unemployment rate now below 4%, the Fed appears ready and willing to tighten financial conditions which was confirmed by the FOMC meeting minutes released this past week. This means there is growing potential for the end of Fed asset purchases in March 2022 AND rate “liftoff” for an interest rate increase. On top of this, what has sparked even further concern is the Fed discussions of potentially attempting to reduce the size of their balance sheet as well during this summer.

There is a widely spoken phrase of “don’t fight the Fed” which I think works both ways. It appears that in 2022, the Fed will at least begin to tighten and we will see how this shift in policy stance will be tolerated by the stock market and U.S. economy. For the past 2 years, the market has gotten used to a dovish fed and extraordinary “easy” monetary policy which has led to extraordinary market gains (up 16% in 2020 and 27% in 2021). I anticipate that at least the first 3 months of 2022 will be pretty bumpy as policy normalization occurs which is also in line with seasonal trends. In the meantime, sector flows have come rushing out from high multiple technology stocks (i.e. anything that is valued using price sales (P/S) ratio), solar, and biotech stocks and has primarily been put into financials (banks and insurance companies) and energy names (not the clean kind but “dirty” oil names). This got me thinking of where we may potentially be in the economic cycle as we begin 2022, especially since historically, inflation hasn’t be able to be reversed lower out of the U.S. economy without an actual economic recession. The leading market groups appear to indicate that we may in fact be somewhere in a late bull in the cycle. What continues to amaze me is two things; 1) the divergence between the market indexes and individual names and 2) how well the Cathie Wood ARKK Innovation ETF is tracking the path of the post 1999/2000 internet bubble. Consider this fact: 40% of the Nasdaq index’s components have fallen by 50% from one-year highs. For reference, at the March 2020 COVID-19 lows, this percentage stood at 60% and the 40% decline level stands at the top 13% of all days since 1999. So far, the indexes, held up namely by the big “FANG” names (Amazon, Apple, Google, etc.) have not experienced the degree of carnage happening within individual Nasdaq names. So my question heading in 2022 is whether the indexes will finally “catch up” to the underlying damage in individual names and we have a > 10%+ correction or is passive investing inflows just simply too strong to allow for this to happen or will the Fed back off its hawkish shift?

Chart Overlay of Nasdaq 100 Post Internet Bubble Collapse to Present Day ARKK Innovation ETF ($ARKK)

Some interesting charts from this past week:

1) Apple iPhone Study

According to a recent survey by Piper Sandler of Gen Z indicates that almost 87% of US teenagers own an iPhone and 88% of teenagers say their next phone will be an iPhone. Pretty “sticky” business!

2) Mortgage Rate Update

In 2021, the US average 30-year fixed mortgage rate was under 3 percent, the lowest annual average in at least half a century. The average rate for a 30-year fixed-rate loan was 3.22%, up from 3.11% last week, according to mortgage finance giant Freddie Mac.

3) Electric Vehicle Battery Metals

Due to the expected transition to electric vehicles over the next 20 years, check out the projected metal demand needed for electric vehicle battery production. Major beneficiaries include copper, aluminum, phosphorus, iron, and manganese.

Stocks I’m Watching

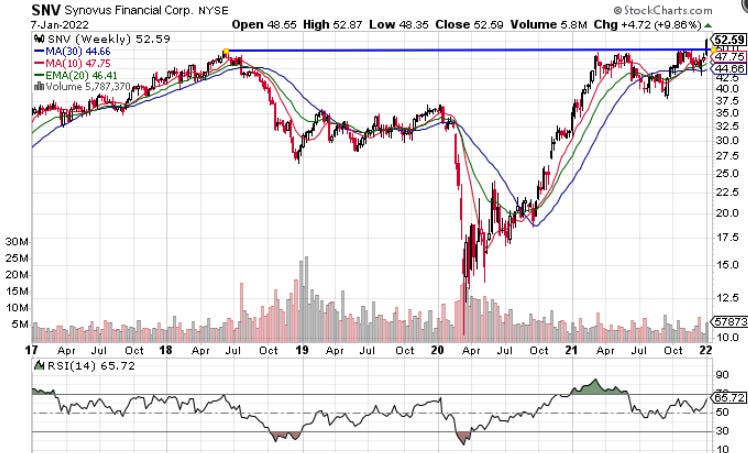

1) Synovus Financial Corp (SNV)

Synovus Financial Corp. operates as the bank holding company for Synovus Bank that provides commercial and retail banking products and services. It operates through three segments: Community Banking, Wholesale Banking, and Financial Management Services. The company’s commercial banking services include treasury management, asset management, capital market, and institutional trust services, as well as commercial, financial, and real estate loans. Its retail banking services comprise accepting customary types of demand and savings deposits accounts; mortgage, installment, and other consumer loans; investment and brokerage services; safe deposit services; automated banking services; automated fund transfers; Internet-based banking services; and bank credit and debit card services. The company also offers various other financial services, including portfolio management for fixed-income securities, investment banking, execution of securities transactions as a broker/dealer, and financial planning services, as well as provides individual investment advice on equity and other securities.

Synovus is a top JP Morgan regional banking pick that was upgraded to overweight in December and recently broke out of a massive weekly base dating back to the beginning of 2018. Last week, as part of its strategy to bring digital- and mobile-banking experiences to its customers, Synovus Financial Corp. has introduced a mobile virtual commercial Visa branded credit cards. Synovus is benefiting from its focus on strategic initiatives, better credit quality and higher interest income. Synovus is also rationalizing its branch network and expects to close four branches in the fourth quarter, bringing the total consolidations to 20 locations since the beginning of 2020. Through these initiatives, SNV expects to achieve pre-tax run rate benefits of an additional $75 million, comprising $20-$30 million of expense savings and $45-$55 million of revenue benefits by 2022 end.

2) Royal Bank of Canada (RY)

Royal Bank of Canada operates as a diversified financial service company worldwide. The company’s Personal & Commercial Banking segment offers checking and savings accounts, home equity financing, personal lending, private banking, indirect lending, including auto financing, mutual funds and self-directed brokerage accounts, guaranteed investment certificates, credit cards, and payment products and solutions; and lending, leasing, deposit, investment, foreign exchange, cash management, auto dealer financing, trade products, and services to small and medium-sized commercial businesses.

A major player in the Canadian banking sector, RBC trades at 12.5X its expected 2022 earnings and has a 3.4% dividend yield. Last week, RBC moved out of its base on increased volume as financials continued to respond to expectations for higher Federal Reserve interest rates. The company estimates that a 25 basis-point increase in interest rates across the curve could result in over $250 million of additional revenue over the next 12 months. In addition, for the year ended October 31, 2021, RBC’s net income grew by 40.3% to C$16.1 billion (~$12.7 billion), following an improvement in its credit quality outlook. In November 2021, Canada’s banking regulator’s decision to lift restrictions on the capital distributions of the country's financial firms, RBC increased its quarterly dividend per share by 11% to C$1.20 (~$0.95). On top of this, the bank announced a share repurchase plan to buy back up to 45 million of its common shares, which could reduce its share count by just over 3% over the next 12 months.

3) Webster Financial Corp (WBS)

Webster Financial Corporation operates as the bank holding company for Webster Bank, National Association that provides a range of banking, investment, and financial services to individuals, families, and businesses in the United States. It operates through three segments: Commercial Banking, HSA Bank, and Community Banking. The Commercial Banking segment provides lending, deposit, and cash management services to middle market companies; and commercial and industrial lending and leasing, commercial real estate lending, equipment financing, and asset-based lending, as well as treasury and payment services.

Webster is another regional bank that experienced a strong weekly breakout out of a massive base dating back to late 2019. Webster is in process of completing a “merger of equals” with Sterling Bancorp which is expected to close soon on February 1, 2022. Management expects to save around $120 million in costs following the merger and the biggest opportunity from the deal is Webster extending its franchise into the NYC metro area. Webster’s net interest margin will likely also benefit from the anticipated hike in interest rates and offers a dividend yield of 2.7%. In addition, the company's interest-bearing deposits with other banks surged to $2,442.8 million at the end of September 2021, from $60.3 million at the end of September 2020.

Disclaimer:

All investment strategies and investments involve risk of loss. Nothing contained in this website should be construed as investment advice. Any reference to an investment's past or potential performance is not, and should not be construed as, a recommendation or as a guarantee of any specific outcome or profit.