Weekly Stock Bullfinder - Week of 1/15

Weekly Stock Bullfinder - Week of 1/15

Stocks I'm Watching - Week of 1/15

Hope everyone had a nice weekend!

New Year, New Bull Markets

As we begin 2024, the past few week have been consumed with media chatter over the launch of new bitcoin ETF’s with predictions this would unleash a new bitcoin bull market, meanwhile price action in different market sectors have been off to surprisingly strong starts. Regardless of your favorite market prognosticators’ forecast for 2024 (up, down, or sideways), catching emerging waves in the start of each year, especially paying attention to volume and price, can lead to significant outperformance. For example, if you recall back to January 2023’s earnings call season, it featured an eye opening proclamation from Microsoft CEO Satya Nadella that “We [Microsoft] fundamentally believe the next platform wave will be AI” which came exactly one day before Microsoft announced its rumored $10B investment in OpenAI. The AI thematic was for 2023, and continues to be, one of most followed technology thematics that produced outperformance in winners such as Microsoft and semiconductor names like Nvidia (NVDA), Super Micro Computer (SMCI), among others. This was primarily due to secular growth in all things AI that was supported by raised earnings guidance while the market rewarded what it perceived as those winners benefitting from this thematic shift. While just a few weeks into 2024 and prior to the full swing of earnings season, a few thematics may already be emerging so far in the early innings of 2024.

Uranium

While conventional oil and gas names have had fits and starts of outperformance during portions of 2022 and 2023, the uranium energy sector, led by market leader Cameco Corporation (CCJ), is seeing renewed accumulation and gains so far in 2024. The relative chart to the SPY below shows that the uranium mining ETF had a powerful weekly breakout last week fueled by news that the world's largest uranium producer, Kazakhstan's Kazatomprom, expects to have production shortfalls over the next 2 years because of shortages of sulfuric acid, which is essential to extract uranium from ore. This news is coupled by recent announcements by China, UK, France, and Japan that they expect heavy investment through 2050 (at the UN Framework Convention on Climate Change, known as COP28, 24 nations pledged to triple nuclear power capacity by 2050) to grow their nuclear power output. A perfect combination for higher commodity prices, already tight supply and increased demand, appears to be unfolding as uranium spot prices have already hit a 15 year high and are moving higher. As a result, notable names like NexGen Energy (NXE), Uranium Energy Corp (UEC), among others, are also having weekly base breakouts on high relative accumulation volumes.

BioTech M&A

The year 2023 saw $178B in Biotech M&A deals which was the best since 2019 with $42 billion of that deal volume happening after Thanksgiving as interest rates began to pull in on softer inflation news and forecasts of Federal Reserve interest rate cuts. The biotech M&A momentum has carried through so far in January as the XBI biotech ETF has just witnessed the best 2-month stretch EVER for the sector as it has seen 8 consecutive weeks of gains, up +14% in November and +18% more in December, or 39% off the October lows. Biotech M&A deal activity started off with a boom in the first week of January with notable M&A deals including Johnson & Johnson paying $2B for Ambrx Biopharma (AMAM) or a 105% premium and Merck paying $680M for Harpoon Therapeutics (HARP) for a a 118% premium. Will the sector M&A dealmaking continue? EY’s analysis suggests it may with its annual “Firepower Report” suggesting that entering 2024, the top 25 pharma companies identified by EY have an estimated $1.37 trillion on hand to make deals. In the 10 years that EY has performed the analysis, it is the second-most-dry powder available at the start of a year. Coupled with forecasted falling interest rates this year (JP Morgan during its earnings call last week has forecasted 6 Fed rate cuts this year), could lead to a high volume M&A year for a sector that needs to address looming revenue challenges over the next five years including the oncoming losses of exclusivity of several blockbuster drugs, the price reduction effects of the Inflation Reduction Act, and an uptick in late-stage clinical trial failures.

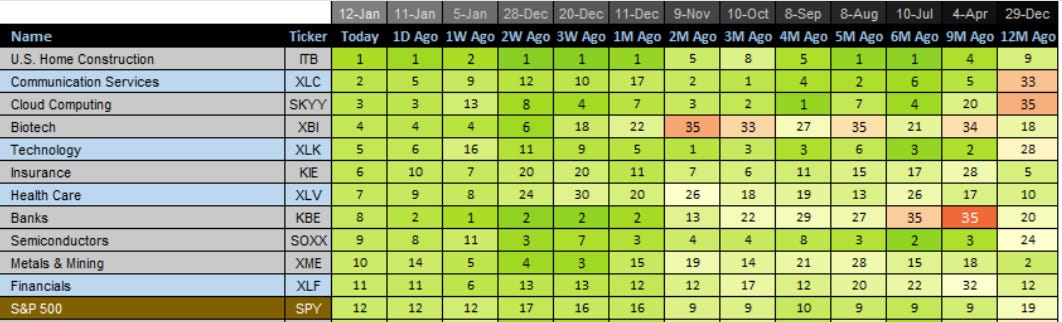

Relative Strength Update

Compared to 3 weeks ago, the healthcare (XLV) sector shows the biggest relative strength increase up 23 spots meanwhile insurance (KIE) and biotech (XBI) also saw notable increases both moving higher 14 spots. Not shown but consumer discretionary (XLY) showing the biggest drop moving down 17 spots.

Quotes of the Week

1) “The U.S. economy continues to be resilient, with consumers still spending, and markets currently expect a soft landing. It is important to note that the economy is being fueled by large amounts of government deficit spending and past stimulus. There is also an ongoing need for increased spending due to the green economy, the restructuring of global supply chains, higher military spending and rising healthcare costs. This may lead inflation to be stickier and rates to be higher than markets expect. On top of this, there are a number of downside risks to watch. Quantitative tightening is draining over $900 billion of liquidity from the system annually, and we have never seen a full cycle of tightening. And the ongoing wars in Ukraine and the Middle East have the potential to disrupt energy and food markets, migration, and military and economic relationships, in addition to their dreadful human cost. These significant and somewhat unprecedented forces cause us to remain cautious. While we hope for the best, the past year demonstrated why we must be prepared for any environment.”

-Jamie Dimon, CEO JP Morgan Chase (JPM)

2) “…For the full year, we reported earnings of $6.25 per share, the second highest EPS result in our history on revenue that was 20% higher than the prior year. We delivered an 11.6% operating margin and pre-tax income of $5.2 billion, a near doubling over 2022. We generate free cash flow of $2 billion while investing $5.3 billion back into the business, and we improved our leverage by two full turns and reinstated our quarterly dividend. Sharing our financial success is a long-standing pillar of Delta’s culture, and I’m thrilled to announce that we’ll be rewarding our employees with $1.4 billion in well-earned profit sharing on Valentine’s Day. For our employees, the estimated payout will be approximately 10% of eligible 2023 compensation, about double of what last year’s payment was. I expect our profit sharing payments will be more than our three largest competitors combined.”

-Ed Bastian, CEO Delta Air Lines (DAL)

3) “Infrastructure is a $1 trillion market forecasted to be one of the fastest-growing segments of private markets in the years ahead. A number of long-term structural trends support an acceleration in the infrastructure investments. These include increasingly growing global demand and upgrading digital infrastructure like fiber broadband, cell towers and data centers. Renewed investments to logistical hubs such as airports, railroads, shipping ports as supply chains are rewired, and a movement towards increased energy independence in many parts of the world, supported by de-carbonization infrastructure. In the United States and around the world, there's a public need for greater investment in infrastructure. This growing needs creates significant investment opportunity for clients. The unprecedented need for new infrastructure, coupled with the record high government deficits means that private capital will be needed like never before. That supply-demand imbalance creates compelling investment opportunities for our clients. At the same time, corporates are looking to engage partners in new projects or partially de-risking the existing ones. These dynamics offer clients, especially those investing for retirement the high coupon inflation-protected long duration investments they need, and we believe it will define the future of asset management for the next 20 years.”

-Larry Fink, CEO Blackrock (BLK)

Some interesting charts from this past week:

1) Red Shipping Attacks- Return of Goods Inflation?

Repeated attacks on marine shipping vessels in the Red Sea have resulted in most shipping companies now avoiding the Red Sea and instead taking longer voyages around Africa’s Cape of Good Hope to reach their final destinations. Meanwhile, the longer voyages and spiking insurance costs have also caused the Shanghai Freight Cost index to surge almost 84% higher over the past month. Overlayed against the Fed’s preferred PCE inflation metrics, the increased shipping costs suggest we will see higher goods inflation readings ahead with a lag of anywhere from 3-6 months. The World Bank is also now warning that the Red Sea crisis could cause surging energy prices, slower growth and higher inflation as new Houthi threats increase supply chain disruption to world trade. For context, we are still 1/4 of where Shanghai freight costs got to back in peak Covid pandemic times.

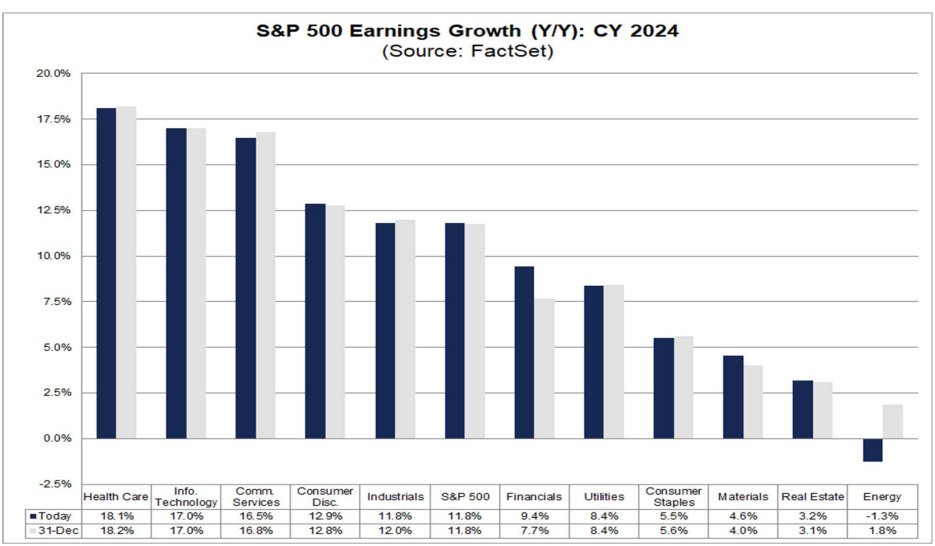

2) 2024 Earnings Growth- FactSet Estimates

Wall St. analysts analysts expect the S&P 500 to report double-digit earnings growth in 2024. The estimated YoY earnings growth rate for 2024 currently stands at 11.7%, which is above the trailing 10-year average annual earnings growth rate of 8.4%. Five of these sectors are projected to report double-digit earnings growth led by the Health Care, Information Technology, and Communication Services sectors.

3) AI Software Growth Estimates

According to estimates from International Data Corporation (IDC), the global AI software revenue opportunity is projected to reach $944bn by 2027, +153% vs 2022 levels, at a compound annual growth rate (CAGR) of 31.4%. The IDC survey found that, in the next 12 months, roughly a third of respondents believe that organizations will prefer to buy AI software from a vendor or use in-house support alongside vendor-supplied AI software for specific use cases or application areas. Investment in Artificial Intelligence Platforms software is anticipated to have a 35.8% CAGR over the 2023-2027 forecast period and presents the largest revenue category. AI Platforms facilitate the development of artificial intelligence models and applications, such as intelligent assistants that can mimic human cognitive abilities.

Stocks I’m Watching

Honorable mentions that didn’t make the final cut: WIRE, SMLR, MPC, CRDO, NTAP, MOH METC, EPAM, NU, EU, QUIK, MNDY, MTH, MLTX, IMVT, WDFC, IPAR, INTR, ESEA, INSW, HUBB,URNM, EU, PPH, CB, PRU, GILD, STNE, ABBV, CAMT, BWXT, BFAM, OSW, WWD, IZM, CELH, ALAR, CPLP, PBPB, IRON, TRAK, SMLR, ACMR, AME, HDSN, TROW, INFY, TIPT, EADSF, DRS, INTA, MMYT, CRDO, MSBHF, SSUMY, AB, KKR, TXT, TFII, CCJ, PIPR, DT, WIRE, VRNS, CTSH, RDNT, IMCR, UBER, UEC, GSL, INSW, BRO, DBRG, WIX, MLM, AB, URA, LEU, CB, MUSA, PDD, QTWO, IMCR

1) Stryker Corporation (SYK)

Stryker Corporation operates as a medical technology company which operates through two segments, MedSurg and Neurotechnology, and Orthopaedics and Spine. The Orthopaedics and Spine segment provides implants for use in hip and knee joint replacements, and trauma and extremities surgeries. The MedSurg and Neurotechnology segment offers surgical equipment and surgical navigation systems, endoscopic and communications systems, patient handling, emergency medical equipment and intensive care disposable products, reprocessed and remanufactured medical devices, and other medical device products that are used in various medical specialties.

Stryker announced in a press release on 1/8 that its 2023 sales surpassed $20B for the first time in its history. Wall St. investment bank Baird picked Stryker as one of its top medtech picks in 2024 as it expects the company’s margins will benefit in 2024 from “premium” prices tied to its MedSurg product launches along with “solid orthopedic end-market demand trends and continued robot-driven core ortho share gains.” Stryker has been a consistent med-tech compounder as it has returned 13.7% per year since 1999, outperforming both the healthcare sector and SPY by 5% over that timeframe. Stryker has also seen a positive to negative ratio of 23-1 for earnings revisions over the past 90 days (2024 and 2025 are expected to see 11% EPS growth) and had a weekly base breakout last week as it looks for a follow through move in the coming weeks as moving averages play catch up.

2) AllianceBernstein Holding L.P. (AB)

AllianceBernstein Holding L.P. is a publicly owned investment manager. The firm is a related adviser The firm manages separate client focused portfolios for its clients. The firm primarily invests in common and preferred stocks, warrants and convertible securities, government and corporate fixed-income securities, commodities, currencies, real estate-related assets and inflation-protected securities.

Asset managers have benefited from stronger than expected inflows as names such as T Rowe Price and others are sporting signs of waking up from deep 2 year downward price channel corrections. AB announced that AUM rose 4.2% to $725B at Dec. 31, 2023 from $696B at Nov. 30, 2023. Cowen recently named AB as one of its financial ‘top picks’ for 2024 as it stated “No question, AB’s MLP structure – and high inside ownership – likely reduces institutional investor interest, though quickly shifting interest rates backdrop may enhance high distribution yield relative appeal. We see clear, identifiable milestones over the next six to 18 months that should help AB outperform the sector”. While currently sporting a 8% dividend yield, AB is expected to grow EPS ~15% in 2024 and 2025. AB is flashing signs of breaking its weekly downtrend resistance as weekly RSI has now climbed above 60 and rising as it looks for a follow through move ahead.

3) Applovin (APP)

AppLovin Corporation engages in building a software-based platform for mobile app developers to enhance the marketing and monetization of their apps in the United States and internationally. The company’s software solutions include AppDiscovery, a marketing software solution, which matches advertiser demand with publisher supply through auctions; Adjust, an analytics platform that helps marketers grow their mobile apps with solutions for measuring, optimizing campaigns, and protecting user data; MAX, an in-app bidding software that optimizes the value of an app’s advertising inventory by running a real-time competitive auction; and Wurl, a connected TV platform, which primarily distributes streaming video for content companies.

Wall St. analysts are very bullish for Applovin’s AXON 2 AI advertising technology engine and investments that Applovin is making to deploy this technology to connected TV over coming quarters. HSBC has a “buy” rating on AppLovin in its digital marketing coverage touting AppLovin’s market leadership in mobile app install advertising and leadership in AI advertising solutions. While currently trading at 21X forward P/E and 13% free cash flow yield, AppLovin’s consensus EPS growth estimates for FY24 and FY25 call for 79% and 23%, respectively. AppLovin’s weekly chart has been consolidating in a tight pattern since August. Positive advertising spend news from Netflix, Meta, and others could lead to a pre-earnings runup. Earnings expected 2/14.

Disclaimer:

All investment strategies and investments involve risk of loss. Nothing contained in this website should be construed as investment advice. Any reference to an investment's past or potential performance is not, and should not be construed as, a recommendation or as a guarantee of any specific outcome or profit.