Weekly Stock Bullfinder - Week of 1/22

Weekly Stock Bullfinder - Week of 1/22

Stocks I'm Watching - Week of 1/22

Hope everyone had a nice weekend!

Semiconductor Arms Race- Wall St. Analysts Still Playing Catch Up

“Some updates on our AI efforts. Our long term vision is to build general intelligence, open source it responsibly, and make it widely available so everyone can benefit. We're bringing our two major AI research efforts (FAIR and GenAI) closer together to support this. We're currently training our next-gen model Llama 3, and we're building massive compute infrastructure to support our future roadmap, including 350k H100s by the end of this year -- and overall almost 600k H100s equivalents of compute if you include other GPUs. Also really excited about our progress building new AI-centric computing devices like Ray Ban Meta smart glasses. Lots more to come soon.”

-Mark Zuckerberg , CEO Meta Platforms

This past week market participants were again caught offsides with the breakneck pace of investments being made to advance all things artificial intelligence (AI). First, came global semiconductor bellwether Taiwan Semiconductor’s (TSM) earnings release in which CEO C C Wei told investors that they expect global semiconductor revenues will climb at least 10% this year marking a turnaround from a 2% drop last year. In addition, TSM provided a bullish capital expenditure forecast of $28 billion to $32 billion in 2024, vs. the $30.45 billion it spent in 2023. This year, TSM has signaled that AI applications on personal consumer devices such as smartphones will drive semiconductor growth with the installation of new features such as live voice and text translation and enhanced image search. We are already seeing this put into motion as the Samsung Galaxy S24 series will be a hybrid AI device (Samsung expects Galaxy AI to be deployed to about 100 million Galaxy smartphones) using both on-device and cloud-based AI. Expect Apple to follow suit later this year with iPhones. Next came Meta CEO Mark Zuckerberg’s announcement that “AI will be our biggest investment area in 2024” with combined engineering and compute resources. Meta has plans to end the year 2024 with over 350,000 Nvidia H100 graphics cards which Wall St. analysts expect will cost Meta as much as $18 billion by the end of 2024. Meta has not been shy in its capital spending; in 2022, Meta spent about $13 billion in investments for building out its metaverse Reality Labs division. As shown in the chart below, Omdia estimates that Nvidia sold 150K H100 chips to both Microsoft and Meta in 2023, while other big tech companies such as Oracle, Amazon, Alphabet, and other also are making heavy investments.

Finally, to cap off the week, Super Micro Computer (SMCI), a provider of rack-scale, AI and Total IT Solutions, announced a massive earnings guidance raise indicating that sales would be expected to be between $3.6 billion to $3.65 billion in its second fiscal quarter ended Dec. 31, up from its prior guidance of $2.7 billion to $2.9 billion, and adjusted earnings would be between $5.40 and $5.55 a share, higher than its previous range of $4.40 and $4.88. This guidance raise resulted in SMCI rocketing 36% higher on Friday. Already, the widely followed semiconductor ETF (SMH), is up 7% YTD. Liquid semiconductor leadership continues to come in the form of Microsoft (MSFT), Broadcom (AVGO), Nvidia (NVDA), AMD, Lam Research (LRCX) and Super Micro Computer (SMCI), among others.

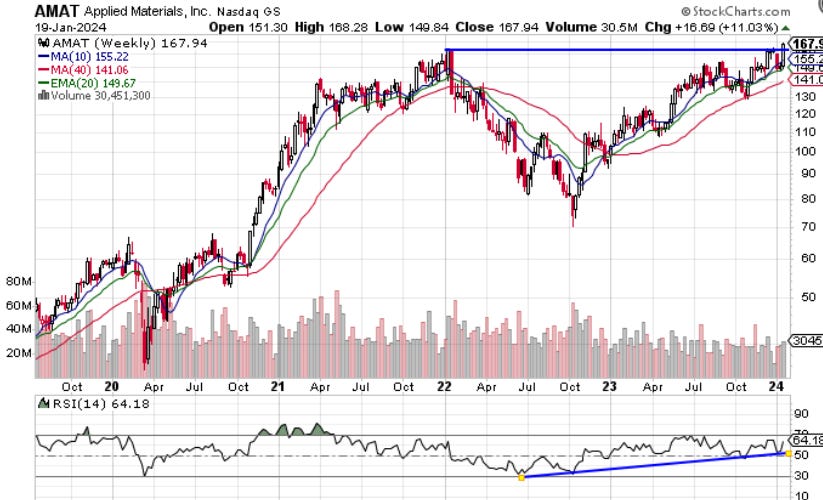

What has become very clear over the past year ever since Microsoft CEO Satya Nadella’s announcement in January 2023 that “AI will become the next platform wave”, Wall St. analysts are continuing to scramble and play catch up to the breakneck speed of investments which are being made by various companies to build out AI services, software and applications, and high performance computing capacity. Even Mark Zuckerberg’s comments this week suggest that the technology “arms race” for high performance computing, powered by advanced semiconductors, remains unabated and supply chain still has not caught up as Nvidia H100 servers are backordered 36 to 52 weeks. Nothing really has changed since Nvidia’s jaw dropping guidance raise in May 2023 which has led to significant investor alpha for those placing shrewd investment bets throughout the AI semiconductor supply chain for companies strategically benefiting from this secular growth story. This upcoming Wednesday and Thursday, ASML, Lam Research, and KLA Corporation, will all provide a look into how the semiconductor equipment and tooling supply chain orders are shaping up to support the AI thematic. Importantly, Lam Research (LRCX) and KLA Corporation (KLAC) have already broken out, while Applied Materials had a weekly base breakout last week on high volume and looks primed for higher prices in coming weeks (earnings 2/16).

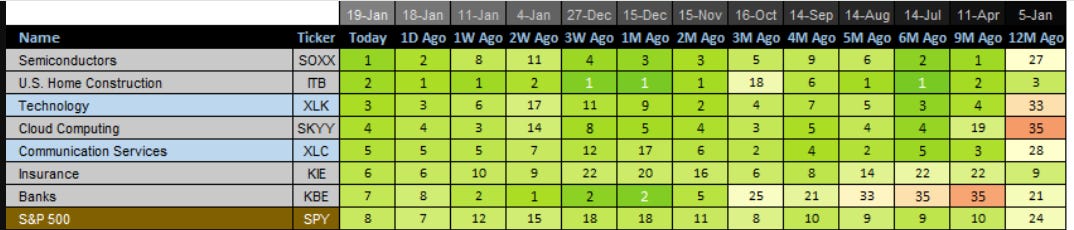

Relative Strength Update

Compared to three weeks ago, a big relative strength increase has been seen in the insurance (KIE) sector moving up 16 spots. This comes after a blowout earnings report from Traveler’s (TRV) this past week. Semiconductors (SOXX) regains the top pole position.

Quotes of the Week

1) “Now I will talk about the AI-related demand….The surge in AI-related demand in 2023 supports our already strong conviction that the structural demand for energy-efficient computing will accelerate in an intelligent and connected world. TSMC is a key enabler of AI applications. No matter which approach is taken, AI technology is evolving to use more complex AI models, as the amount of computation required for training and influence is increasing. As a result, AI model need to be supported by more powerful semiconductor hardware, which requires use of the most advanced semiconductor process technologies…..the value of TSMC technology position is increasing and we are well-positioned to capture the major portion of the market in terms of semiconductor component in AI. To address unassessable AI-related demand for energy-efficient computing power, customers rely on TSMC to provide the most leading-edge processing technology at scale with a dependable and predictable cadence of technology offering.”

-Wendell Huang, VP and CFO Taiwan Semiconductor Manufacturing Company Limited (TSM)

2) “As you saw in our [press] release, we incurred $53 million of additional costs in the quarter, largely related to higher claims cost and exceeding coverage limits in certain insurance layers. And this, despite 2023 being the Company's best performance in history on safety, measured by having our lowest DOT preventable accidents per million miles. We remain one of the safest carriers in the industry. Yet our insurance rates continued to increase as the industry experiences higher verdicts, and as a result, higher litigation settlements. During verdicts in trucking cases where the verdicts exceed $1 million, have seen an 867% increase in the average size of verdicts from 2010 to 2018. Given that the majority of motor carriers in the industry carry only $1 million in coverage, just above the legal minimum of $750,000 in coverage, it's the larger carriers who bear the brunt or disproportionate share of the escalating insurance and claims cost and ultimately these inflationary costs get passed on to customers and consumers…..On the insurance cost pressure that we're seeing, our general approach to risk management is to maintain coverage and insurance policies for our exposures. And as we reset the premiums going into 2024, we saw upwards of 50% to 60% increases in those premiums. And so when we talk about the inflationary pressures that we're seeing in 2024, it's mostly around our premiums. We've done a great job this year and working and focusing on safety to try to bring those incidents down. But the claims costs of the individual claims is what's driving a lot of the inflationary pressures.”

-John Roberts, CEO J.B. Hunt Transport Services, Inc. (JBHT)

3) “…We provide an outlook for used vehicle values, which declined 9% in 2023 and have declined 26% from their 2021 peak. We are assuming another 5% decline in 2024 with much of that decline occurring in the first half of the year. That would result in a total decline from peak levels of just over 30%. We continue to expect used values will stabilize and ultimately settle around 20% higher than pre-pandemic levels. With new vehicle production below pre-pandemic levels for nearly four years, used supply will remain 15% below historical norms over the next several years and provide structural support for used values.”

-Jeff Brown, CEO Ally Financial Inc. (ALLY)

Some interesting charts from this past week:

1) Texas Construction Projects Heating Up

According to Dodge Data and Goldman Sachs Research, of the more than $1 trillion in manufacturing and infrastructure investments that have been announced and broken ground from 2021-2023, the state Texas comprises more 25% of the projects, with semiconductor and clean energy battery projects comprising the majority of the new investment.

2) Private Auto Insurance- Premium Increases Driving Pain to Consumers

As compiled by S&P Global Market Intelligence, the largest auto insurance companies increased premiums all by double digits last year between 10-18%. Farmers Insurance takes the prize of having the highest increase over the past two years (35%) and 5 year period ended 2023 (55%). The average American driver’s insurance payment has spiked almost 27% in the past two years. On a state basis, drivers in the state of Texas have seen the nation’s largest insurance-rate increase, increasing a shocking 45.5% from just two years ago.

3) Tesla Automotive Margins- Going in Reverse, Will It Revert?

Tesla’s automotive gross margins have become a key investor focus area and have been going in reverse since peaking at 30% in 2Q2022 and dropping down to 16.33% in its most recent quarter. In Tesla’s upcoming earnings release for 4Q23, automotive gross margins are projected to slip ~60bp QoQ and operating margins are forecasted to fall another ~40bp QoQ to 7.2%. The margin slippage is based upon increased global EV competition and a belief that Tesla will be in investment mode in the first half of the year with the ramp in production of Cybertruck along with the Model 3 refresh that will likely dampen margins. Tesla still holds a slight advantage over other automakers who generally trend between 10-14% gross margins but the gap compared to wide automaker industry norms is narrowing. The current Wall St. consensus sees Tesla’s gross margins rising in the second half of 2024 to yield full year 2024 margins of about 18.5%.

Stocks I’m Watching

Honorable mentions that didn’t make the final cut: LEU, WIT, UPWK, BAH, DRS, PGNY, JEF, PSN, ACLX, PDD, AER, EU, RMBS, TJX, L, CB, VCEL, QUIK, ACIC, EXLS, TWST, CRH, FAST, BLDR, ESEA, FERG, WSM, ORLY, AZO, PSTG, TPX, TARO, TRMD, KRYS, DT, HLT,MAR, MLM, NAIL, XHB, ORCL, AMAT, DT, TREX, ACN, STNG, INSW, TRMD, ASC, NOW, CPRT, ALLY, IMOS, BN, CB, ARCH, ESNT, RLI, STNG, ASML, AMAT, MELI, ALLY, WIRE, INTU, MCD, TOL, XHB, HUBB, ESNT, KKR, BRK/B, ATR, ESI, EXPE, MRK, CSX, GSL, BN, HUBS, NOA, SIGI, TOL, MLI, TPH, CNXC, GNK, STX, BLK, MPWR, FROG, JEF, LIN

1) Euroseas (ESEA)

Euroseas Ltd. provides ocean-going transportation services worldwide. The company owns and operates containerships that transport dry and refrigerated containerized cargoes, including manufactured products and perishables.

Euroseas is emerging out of a multi-year weekly base breakout dating back to August 2021 and is benefiting from a strong combination of 7 new feeder vessels delivering in 2024 (5 of which will deliver by 2Q2024) and surging spot shipping rates (TCE) as a result of ship re-routings around the Cape of Good Hope. In addition, Euroseas has a lower charter lockup percentage (70%) in 2024 leaving it exposed to benefit at just the right time for higher TCE rates. Euroseas remains highly profitable with 39% net income margins, forward P/E of 2X, and sports a 5% dividend yield. Similar to 2021, if TCE’s continue to rise (the Harpex index is now 28% higher than it was in January 2019, pre-COVID and it now costs on average $3,030 to send a container from Shanghai to Europe, up from $707 in mid-November), Euroseas stands to benefit and could continue to re-rate. Pullback to a rising 10WK moving average could offer an entry opportunity.

2) Red Rock Resorts (RRR)

Red Rock Resorts, Inc., through its interest in Station Holdco and Station LLC, develops and operates casino and entertainment properties in the United States. It operates through two segments, Las Vegas Operations and Native American Management.

Red Rock Resorts is seeing bullish commentary and glowing reviews around its new Durango Casino and Resort property, its first new casino in 15 years, which it opened in December 2023 and is aimed squarely at the Las Vegas locals market. CBRE Equity Research has forecasted Durango to ramp to a 20%+ ROI over the next 2-3 years. Consensus estimates for Red Rock calls for 44% EPS growth on 25% free cash flow margins in FY24. Nevada casinos as a whole are riding a hot steak, with 33 straight months of statewide gaming revenue of at least $1 billion in the books. Recently, Macquarie issued an Outperform rating on Red Rock Resorts and price target of $58 ahead of its earnings report as analyst Chad Beynon believes “RRR is one of the most sophisticated operators with some of the highest margins and strong underlying demographics/wage growth.” From a technical perspective, Red Rock is emerging out of a long weekly base extending back to October 2021 and looks primed to follow through in coming weeks with a strong earnings report. Earnings are expected February 7th.

3) W.R. Berkley (WRB)

W. R. Berkley Corporation, an insurance holding company, operates as a commercial lines writer in the United States and internationally. It operates in two segments, Insurance and Reinsurance & Monoline Excess.

W.R Berkley had a weekly breakout last week ahead of its upcoming earnings this week as the broader insurance sector is benefiting from passing through strong insurance premium prices combined with surging investment income stemming from a higher interest rate environment. Travelers Insurance reported strong earnings last week which provided a tailwind to the broader insurance group. Higher interest rates have provided a significant tailwind to investment income as last quarter Berkley reported an average annualized book yield on its fixed-maturity portfolio of 4.2% through Q3, up from 2.6% in 2022, resulting in net investment income surging higher to $739 million in the period, up from $548 million in 2022. W.R. Berkley also has a history of consistent operating profitability, averaging a combined ratio of 93.2% over the past ten years and has produced favorable shareholder returns paying out a $0.50/share special dividend just last quarter. Consensus estimates for FY24 call for 19% EPS growth and 23% free cash flow margins with forward P/E of 13X. Earnings expected 1/24.

Disclaimer:

All investment strategies and investments involve risk of loss. Nothing contained in this website should be construed as investment advice. Any reference to an investment's past or potential performance is not, and should not be construed as, a recommendation or as a guarantee of any specific outcome or profit.