Weekly Stock Bullfinder - Week of 2/19

Weekly Stock Bullfinder - Week of 2/19

Stocks I'm Watching - Week of 2/19

Hope everyone had a nice weekend!

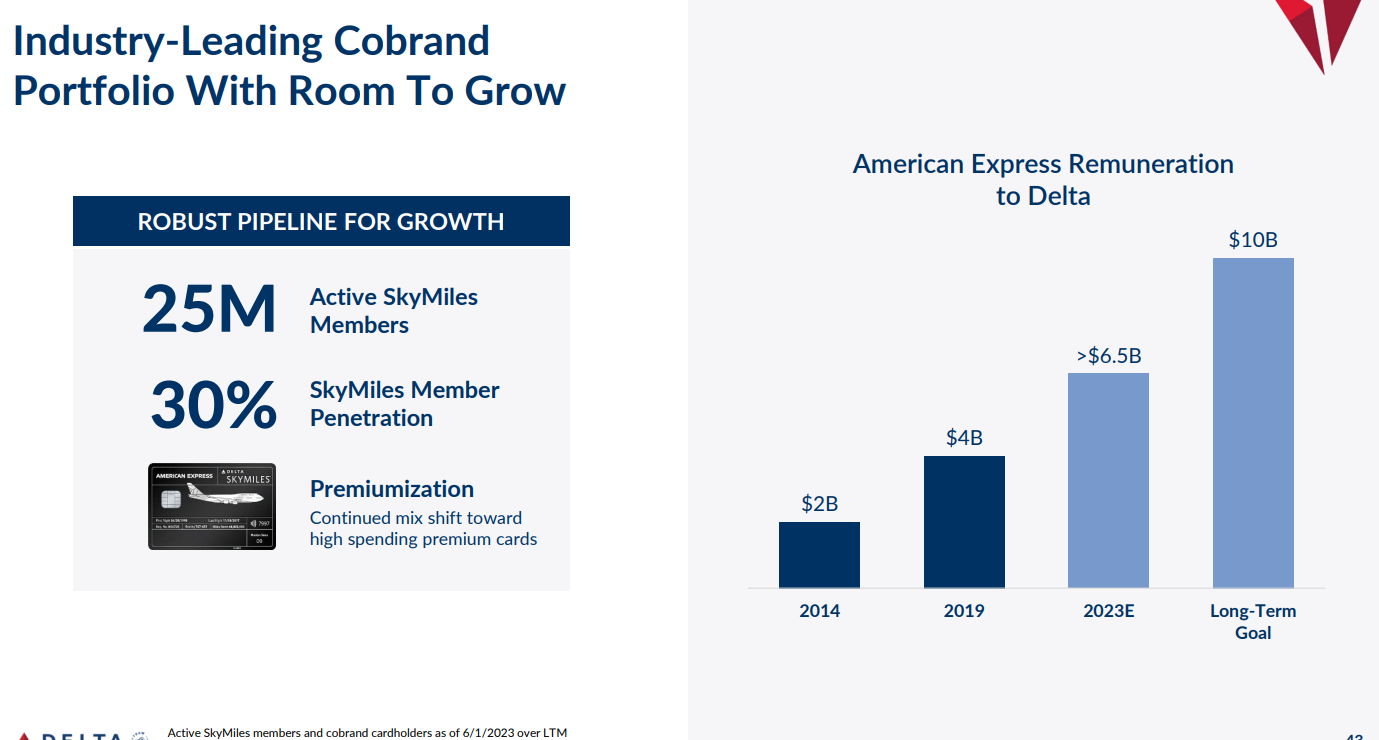

The Loyalty Business

Co-branded credit card usage in the travel industry has become significant source of ancillary revenue, earnings, and cash flow for airline and hotel operators. The airline industry was amongst the first to start offering co-branded credit cards, with hotels soon following suit, and its usage is now widespread throughout the travel industry. Co-branded credit cards are issued with a mutual partnership between a company (i.e. Marriott, etc.) and a credit card issuer and network. They are often backed by a major network and/or a major card issuer (i.e. Visa, Mastercard, AmEx, etc), and consumers can use them anywhere to access special perks like earning loyalty points for redemption. According to research from Airlines for America, approximately 30 million Americans, or 1 in every 4 households, have co-branded airline credit cards.

Loyalty programs have become big business and increasingly valuable:

-According to global advisory firm On Point Loyalty, a valuation analysis of 170 commercial passenger airlines suggests that Delta Airline’s SkyMiles loyalty program has the highest valuation at almost $28B. This valuation is higher than Delta’s total current market capitalization which stands at $25.8M as of Friday’s market close. What makes the loyalty programs so valuable? The key driver of the valuation involves attractive high margins as well as access to the wealth of expanded customer data information including member travel patterns, spending behaviors, and preferences which can be used for personalized marketing and identifying revenue opportunities such as financial services, among others.

-Delta Airlines has 25M global Delta SkyMiles members and Delta is expected to receive almost $7B of remunerated cash flow back from its co-branded credit card deal American Express in 2023. Delta Airlines brought in $1.7 billion under its credit card deal with American Express in its third quarter of 2023, which represents 11% of Delta’s total revenue of $15.5B for the period.

-In June 2023, Delta CEO Ed Bastian explained that when you add up the total spending customers charge via Delta’s American Express cards, it is estimated that it approaches 1% of the U.S. GDP, or roughly $268 billion.

-During the peak of the COVID-19 pandemic in 2020, loyalty programs took on a new life and served as liquidity buffers for the first time ever. Specifically, multiple airlines put their loyalty programs up as collateral to help secure debt financing from Wall Street lenders which also offered a peak behind the curtain as to their underlying economics. In fact, Wall Street lenders valued all of major airlines’ mileage programs higher than the airlines themselves. For example, at the time, United’s MileagePlus program was valued at $22 billion, while the company’s market cap at the time was only $10.6 billion. After pledging United’s MileagePlus program as collateral, United was able to secure a ~$5 billion loan from investment firms Goldman Sachs, Barclays, and Morgan Stanley. Delta Airlines did the same thing which back stopped their $6.5B pandemic loan.

-In 2020, United Airlines completed a presentation on their MileagePlus loyalty program, where they shared that their co-branded credit card contracts with JP Morgan Chase and Visa guaranteed a minimum margin of 20% on the purchase of miles. In addition, they noted that their MileagePlus program generated $1.8B of EBITDA or 26% of total United adjusted EBITDAR. S&P Global Ratings Analyst Philip Baggaley has estimated that between a quarter and a third of the airline’s profits are generated from their loyalty programs.

Relative Strength Update

Biotech (XBI, +8), Retail (XRT, +7), and Transports (IYT, +7) all exhibiting increasing relative strength in recent weeks as semiconductors, home construction, and communication services groups continue holding up strong.

Quotes of the Week

1) “…Let me share our latest perspective on the market environment. In our discussions with customers, we’re hearing that overall market dynamics are improving. There is a reacceleration of capital investment by cloud companies, fab utilization is increasing across all device types and memory inventory levels are normalizing……While major end market inflections, such as AI and IoT, electric vehicles and renewable energy are already driving semiconductor growth and innovation, it’s important to recognize they are still in the early stages of adoption. For example, high-performance GPUs for AI data centers only represent 6% of leading-edge foundry-logic wafer starts today. The full potential of technologies like AI cannot be unlocked without next-generation chips with better performance, power and cost. The technology roadmap for semiconductors is rich with possibilities and opportunities, but also incredibly complex.”

-Gary Dickerson, Chief Executive Officer Applied Materials (AMAT)

2) “…We thought it would be helpful just to provide some thoughts regarding 2024 and how we see things may be progressing. On the new side of the business, as we know vehicle supply is going to continue to return to pre-pandemic levels. And I think leasing and retail incentives are clearly going to pick up through the year but I think will remain below pre-pandemic levels in total. So inventory levels will continue to increase over the course of 2024, but we expect demand to be robust. Battery electric vehicle product introduction and customer interest in these vehicles is clearly going to be a key dynamic this year. As widely reported, bad PVRs consistently fell during 2023 and in most instances, are lower than similar combustion engine vehicles. And as with all things, it's about balance and it does appear OEMs are adjusting their plans and actions to match demand more closely. And frankly, this will be well received. Hybrids are doing well in the marketplace, and we have good exposure to this portion of the market based upon our brand mix, and we expect our new margins to continue to moderate over the course of 2024.”

-Michael Manley, Chief Executive Officer AutoNation (AN)

3) “We gained share, including taking the number one position in combined OSB [Online Sports Betting] and iGaming gross gaming revenue share in the US for the third quarter….We lean heavily on data and analytics, giving us the confidence to cut expenses in some areas and double down in others. This year, our focus will largely be on essentially the same items. We are still in the early innings of the US online gaming industry, and there is still share that can be gained through innovation and operational excellence. We will continue to focus on product and customer experience as key differentiators. Having superior lifetime values and customer acquisition costs is the ultimate competitive advantage. And we have a number of initiatives planned to enhance both in 2024 and beyond. Going into 2024, there are three main opportunities on my mind. The first is continuing to foster our entrepreneurial culture and empower our great people to pursue big opportunities. The second is developing our next crop of leaders and giving them opportunities that allow them to stretch, grow, and contribute at higher levels. The third is leveraging our free cash flow which we expect to generate in order to maximize value for our shareholders.”

-Jason Robins, Co-Founder, Chairman & CEO, Draftkings (DKNG)

Some interesting charts from this past week:

1) Texas and Sunbelt Metro Apartments Supply Surge

According to John Burns Research and Consulting, apartment unit inventory is booming in the US sunbelt with multiple cities such as Charlotte, Austin, Raleigh-Durham, Phoenix, Nashville, and Charleston, all seeing >10% of existing apartment unit inventory now under construction. With deliveries coming over the next 18-24 months, this unit growth should continue to put downward pressure on rent growth. Nationally, apartment units coming out of construction in 2024 is expected to be 672k, the highest annual unit increase since 1974.

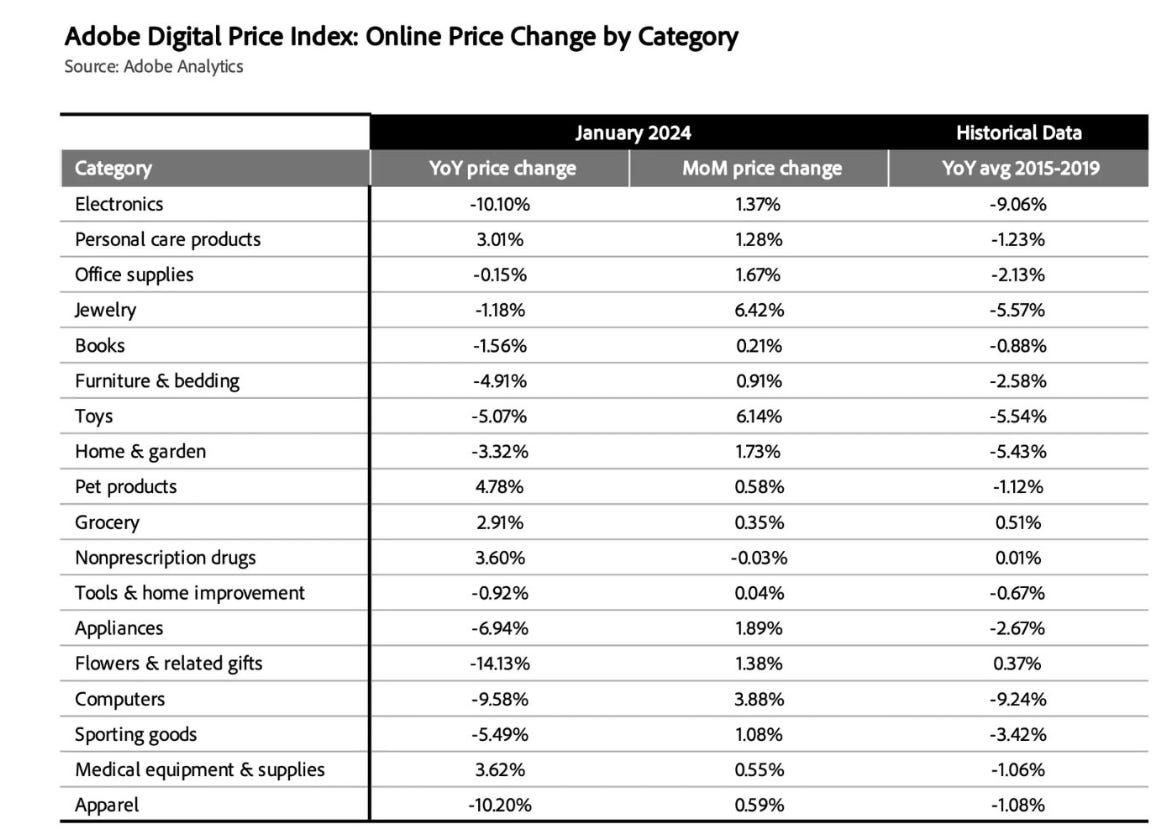

2) Adobe Digital Price Index- January 2024 Update

The Adobe Digital Price Index (DPI) provides the most comprehensive view into how much consumers are paying for goods online using analytics on real time website prices. The DPI covers more than 100 million products in the US and is modeled after the Consumer Price Index (CPI) issued by the US Bureau of Labor Statistics (BLS). The Adobe Digital Price Index showed a 1.4% M/M gain for January, following a 2.4% gain for December 2023. Prices are still down Y/Y in several categories, but goods deflation appears to be easing.

https://business.adobe.com/resources/digital-price-index.html

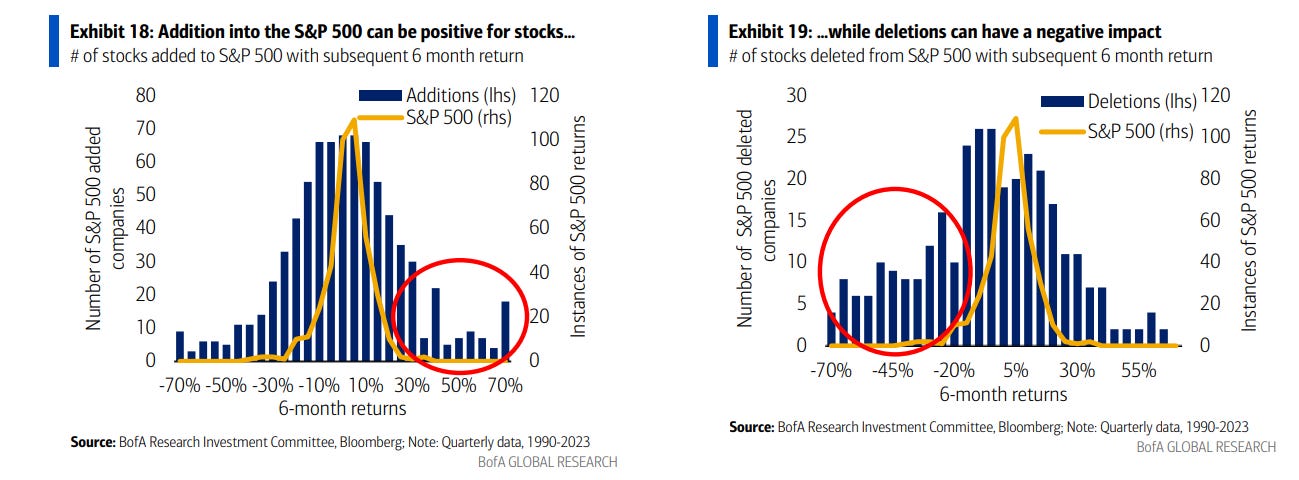

3) S&P 500 Index Member Changes- Impacts to Forward Returns

Company inclusion within an equity index such as the S&P 500 can be an important signal to investors that a stock has high quality earnings and provides strong liquidity. According to Bank of America Global Research, companies added to the S&P 500 since 1990 returned 4.3% (8.7% annualized) on average in the subsequent 6 months with 22 stocks gaining >65%. On the flipside, deleted stocks from the S&P 500 index typically lose 7% in the 6 months following removal. Six stocks were added in 4Q2023 to the S&P 500, including Uber, Jabil, and Builders FirstSource while Sealed Air, Alaska Air Group, and SolarEdge Technologies were removed. Bank of America Global Research expects KKR to be added to the S&P 500 index in the next six months and potentially as early as the March 15th rebalance (announced on March 1st).

Stocks I’m Watching

Honorable mentions that didn’t make the final cut: CELH, MUSA, BXSL, MTDR, TWST, JEF, MNDY, EVR, FANG, DHT, RLJ, TPX, RDNT, H, DKS, ASO, ERJ, LPLA, ROL, CME, FLR, UBER, TMHC, CRDO, MC, GLOB, EPAM, CLBT, TRGP, DHT, WEX, ATI, HTGC, SQSP, XP, HACK, WRB, NVMI, CNTA, VIST, SPG, BLBD, AB, MMC, PXD, PR, CSX, IMO, SIG

1) Viper Energy (VNOM)

Viper Energy, Inc. owns, acquires, and exploits oil and natural gas properties in North America. It owns and acquires mineral and royalty interests in oil and natural gas properties primarily in the Permian Basin.

Energy sector M&A spree continues to remain hot as producers need to replace declining wells and consolidate acreage. This week, Diamondback Energy (FANG), announced a $26B purchase of Endeavor Energy Partners that would make the combined company the third-largest oil and gas producer in the Permian Basin, behind only Exxon and Chevron. During the conference call, it was noted that almost 2/3rd’s of the purchase price related to mineral rights, increasing expectations that Endeavor’s mid-land minerals will likely to be dropped down eventually to Viper Energy, adding more scale (est. 2-3 mBOE) to Viper. Viper has been maintaining a 75% payout ratio and currently sports a 6% forward dividend yield which is flown through 1099-DIV forms as Viper is taxed as a corporation. From a technical perspective, Viper had a weekly base breakout on high volume last week and could offer entry on pullback to rising 10WK moving average.

2) TechnipFMC Plc (FTI)

TechnipFMC plc engages in the oil and gas projects, technologies, and systems and services businesses in Europe, Central Asia, North and Latin America, the Asia Pacific, Africa, and the Middle East.

TechnipFMC is well-positioned in the oilfield services industry, benefiting from the robust growth in international offshore activities. TechnipFMC derives >80% of its revenue from sub-sea operations and 90% of revenue is international. TechnipFMC continues to rack up impressive contract wins; in just the month of January it received a >$1B award from Petrobras for work on its Mero 3 project and a “significant” ($75M-$250M) award from BP for Argos Southwest Extension project in the Gulf of Mexico's Mad Dog field. TechnipFMC's subsea backlog surged last year to $12.1 billion, marking a substantial 58.8% increase from the previous year. Approximately $4.5 billion of backlog is estimated to be liquidated to revenue for the upcoming year and the remaining $6.5 billion earmarked for 2025 and onwards. Trading at forward P/E of 14X, consensus estimates call for EPS growth of 144% and 58% in 2024 and 2025, respectively. From a technical perspective, TechnipFMC has formed a weekly bull flag with its rising 40WK moving average serving as support. Earnings expected 2/22.

3) Ardmore Shipping Corporation (ASC)

Ardmore Shipping Corporation engages in the seaborne transportation of petroleum products and chemicals worldwide.

Ardmore Shipping continues to benefit from surging product shipping rates due to shipping attacks and re-direction from the Suez Canal and low water levels in the Panama canal. After reporting earnings last week, Ardmore raised its dividend by 31% and now sports a forward yield of 5.7%. Ardmore also had a investor day on Thursday and noted that for every $10,000 per day increase in TCE rates, Ardmore’s EPS is expected to increase by approximately $2.30/sh and free cash flow would increase nearly $100 million. Currently, MR TCE rates are trading at ~$35,400/day, which is well above Ardmore’s breakeven rate of $13,900/day and 9% higher than just last quarter. Free cash flow margins for 2024 are estimated at 41%. Jefferies maintained is “buy” rating and $20 PT last week, 25% higher from current levels. From a technical perspective, Ardmore is continuing to build out a weekly cup and handle formation and looks primed to move higher.

Disclaimer:

All investment strategies and investments involve risk of loss. Nothing contained in this website should be construed as investment advice. Any reference to an investment's past or potential performance is not, and should not be construed as, a recommendation or as a guarantee of any specific outcome or profit.