Weekly Stock Bullfinder - Week of 2/26

Weekly Stock Bullfinder - Week of 2/26

Stocks I'm Watching - Week of 2/26

Hope everyone had a nice weekend!

2023 Berkshire Hathaway Shareholder Letter- Buffett Insights

Berkshire Hathaway’s Annual Report release and associated shareholder letter from famous CEO and investor Warren Buffett is always much anticipated Saturday morning reading material. This year’s letter is again filled with antidotes and pearls of investing wisdom gleaned from his multi-decade business career which has seen Berkshire Hathaway shares yield a compounded annual gain of 19.8% from 1965-2023. Below I have highlighted some interesting takeaways from this year’s letter. Link is provided below in case you want to read the full publication.

1) Investments in key U.S. strategic national assets should provide outsized returns over time

Buffett’s letter explains his investment thesis and rationale for making his investments in railroad freight operator Burlington Northern Santa Fe (2009) and recent investments in oil and gas producer Occidental Petroleum (OXY). Buffet explains, “Rail is essential to America’s economic future. It is clearly the most efficient way – measured by cost, fuel usage and carbon intensity – of moving heavy materials to distant destinations. Trucking wins for short hauls, but many goods that Americans need must travel to customers many hundreds or even several thousands of miles away…my guess is that it would cost at least $500 billion to replicate those assets and decades to complete the job.” Buffett explains that although the railroad business is highly capital intensive, the expansive existing physical rail network is highly unlikely to be replicated by a competitor and the transportation efficiencies provide a durable physical investment moat. Regarding Occidental, “We particularly like its vast oil and gas holdings in the United States, as well as its leadership in carbon-capture initiatives, though the economic feasibility of this technique has yet to be proven. Both of these activities are very much in our country’s interest.” Buffett then goes on to explain how the U.S. shale and fracking technology revolution in 2011 is largely responsible for U.S. energy self-sufficiency and how Occidental’s annual oil production approximates the entire inventory of the U.S. Strategic Petroleum reserve. Alluding to Occidental’s U.S. national and strategic energy importance, Buffet states “Occidental is doing the right things for both its country and its owners.” While admitting he “does not know what oil prices will do over the next month, year, or decade” Buffett solely bases his investment thesis focusing on the importance and expected future returns on its oil and gas business and interesting enough is completely silent on Occidental’s “green” initiatives, such as carbon capture, even going so far as saying their economic feasibility as “unproven”. Berkshire also owns a 6.8% ownership stake in oil and gas E&P Chevron (CVX). Reading into this and his recent statements, one can infer that Buffett is highly skeptical that oil and gas energy sources will be quickly displaced in the near future.

2) Investors Should Apply Patience and Sit in “Winners” With Strong Brands, Management, and Buyback Programs

In the section of the letter titled “Non-Controlled Businesses That Leave Us Comfortable”, Buffett explains how Berkshire’s investment inaction, which Buffett calls Berkshire’s “Rip Van Winkle Slumber”, with prior investments made in American Express and Coca-Cola have continued to lead to outsized returns on capital over time. Buffett brilliantly explains several important points during this small section of the letter. First, Buffett explains his dislike in investing in “newcomers” or new IPO’s and talks about Berkshire’s investments were made after both companies established products which “traveled” or established global reach and well after both companies failed in “expanding into unrelated areas". In other words, Buffet recognized the “S-curve” of both businesses and invested in the successful “base business”. Ever since then, Berkshire has sat on their hands while management of both companies has executed strong capital return programs of dividends and share repurchase programs. Buffet concludes, “The lesson from Coke and Amex? When you truly find a wonderful business, stick with it. Patience pays, and one wonderful business can offset many mediocre decisions that are inevitable.” The takeaway thought from Buffett’s letter stresses the importance of feeding your winners and letting them compound without unnecessarily interrupting their compounding by making emotionally driven sales due to market turbulence or other factors.

3) Utility Businesses Are Facing Increasing Hostile Regulatory Environments Threatening Future Investment & Returns

Pages 13 and 14 of the Berkshire Hathaway letter includes Buffett’s lamenting over the hostile regulatory landscape and emerging unfavorable economics of the Berkshire Energy business. In a mea culpa, Buffett writes, “I did not anticipate or even consider the adverse developments in regulatory returns, and, along with Berkshire’s two partners at Berkshire Energy, I made a costly mistake of doing so.” Buffett humbly explains that large unfavorable surprises have emerged in the energy utility sector such as increasing wildfire loss damages and potential changing requirements in certain western US states to require underground transmission for future energy utility projects (which would significantly escalate construction costs and erode project economics). Buffet states “..in such jurisdictions [California and Hawaii], it is difficult to project both earnings and asset values in what was once regarded as the most stable industries in America.” Meanwhile, Buffett states “When the dust settles, America’s power needs and consequent capital expenditure will be staggering.” Thus, while Buffett has lamented the changing and increasing costs of regulatory changes, he nonetheless cites energy production and electrical grid infrastructure spending as secular growth areas that should be expected to see outsized investment in coming years and decades ahead to support U.S. economic growth.

Full Letter & Annual Report Link:

https://berkshirehathaway.com/2023ar/2023ar.pdf

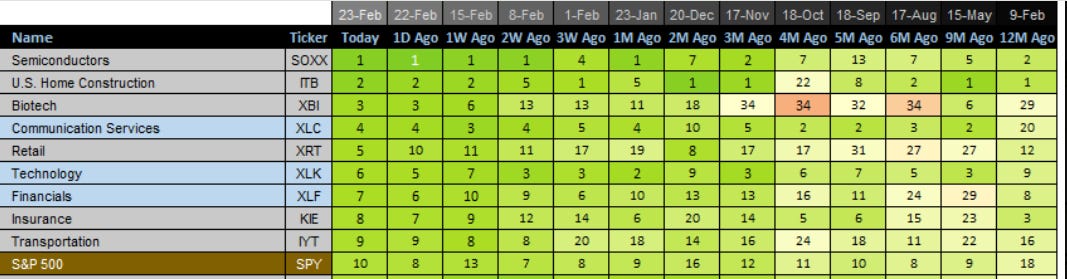

Relative Strength Update

Retail (XRT) and Biotech (XBI) sectors have seen strong relative strength over the past 3 weeks, moving up 12 and 10, spots. Meanwhile, semiconductors and U.S. home construction continue holding the top spots as of last week. Not pictured but telecoms (IYZ) showed the most relative weakness the past 3 weeks moving down 19 spots.

Quotes of the Week

1) “Berkshire’s ability to immediately respond to market seizures with both huge sums and certainty of performance may offer us an occasional large-scale opportunity. Though the stock market is massively larger than it was in our early years, today’s active participants are neither more emotionally stable nor better taught than when I was in school. For whatever reasons, markets now exhibit far more casino-like behavior than they did when I was young. The casino now resides in many homes and daily tempts the occupants. One fact of financial life should never be forgotten. Wall Street – to use the term in its figurative sense – would like its customers to make money, but what truly causes its denizens’ juices to flow is feverish activity. At such times, whatever foolishness can be marketed will be vigorously marketed – not by everyone but always by someone…One investment rule at Berkshire has not and will not change: Never risk permanent loss of capital. Thanks to the American tailwind and the power of compound interest, the arena in which we operate has been – and will be – rewarding if you make a couple of good decisions during a lifetime and avoid serious mistakes”

-Warren Buffett, CEO & Chairman Berkshire Hathaway

2) “I think on the macro, starting with sort of the big picture, I think we continue to believe we are both on a disinflationary path and a path that is consistent with the soft landing in the economy at large. Now things like the CPI print from 1.5 weeks ago, obviously, even though there might be some noise in that metric, obviously, reflect that the so-called last mile will be hard. We should expect that, perhaps bumpy. We have an economy that’s obviously running quite strong, nearly full employment, really a high level of confidence both in most of the consumer segment and also among CEOs. We see that in our own portfolio company CEO surveys. They’ve consistently been actually even more optimistic than the investors over the last year or so, and they’ve largely been proven right. But it’s also an economy that we see is decelerating. We see it in hiring. When we survey our portfolio company CEOs 2 years ago, something like 94% of CEOs said hiring was a problem. It was a challenge in the last quarter. That dipped below a majority below 50% for the first time in that time period….So I think where that leaves us is that with our own internal data, rate cuts will be lower and lighter. It was sort of astonishing that only a month or so ago, the market was supposedly discounting 6 cuts this year. We thought that was very aggressive. So whether that’s sort of in 3 cuts, plus or minus 1, that’s probably a good zone and obviously more second half weighted. So that said, I think in terms of the market and market participants, and we’ll get into sort of deployment, I think that the dynamics are good. I think the cost of capital, with all that I just said, is clearly coming down.”

-Michael Chae, Chief Financial Officer Blackstone, Inc. (BX)

3) “…Fundamentally, the conditions are excellent for continued growth, calendar '24 to calendar '25 and beyond, and let me tell you why. We're at the beginning of 2 industry-wide transitions, and both of them are industry-wide. The first one is a transition from general to accelerated computing. General-purpose computing, as you know, is starting to run out of steam. And you could tell by the cloud service providers (CSPs) extending and many data centers, including our own for general-purpose computing, extending the depreciation from 4 to 6 years. There's just no reason to update with more GPUs when you can't fundamentally and dramatically enhance its throughput like you used to. And so you have to accelerate everything. This is what NVIDIA has been pioneering for some time. And with accelerated computing, you can dramatically improve your energy efficiency. You can dramatically improve your cost in data processing by 20:1, huge numbers. And of course, the speed. That speed is so incredible that we enabled a second industry-wide transition called generative AI….. But remember, generative AI is a new application. It is enabling a new way of doing software, new types of software being created. It is a new way of computing. You can't do generative AI on traditional general-purpose computing. You have to accelerate it. And the third is, it is enabling a whole new industry….. A whole new industry in the sense that for the very first time, a Data Center is not just about computing data and storing data and serving the employees of the company. We now have a new type of Data Center that is about AI generation, an AI generation factory, and you've heard me describe it as AI factories.”

-Jensen Huang, Founder & CEO, NVIDIA Corporation (NVDA)

Some interesting charts from this past week:

1) Indeed Wage Growth Tracker- January 2024 Update

The Indeed Wage Growth Tracker, which is designed to measure changes in the growth in the wages and salaries advertised in job postings, continues to show downward moment in the latest January 2024 update. The Indeed posted jobs wage growth came in at 3.6% in January, continuing its steady decline over the past two years as US labor market normalization continues. Posted wage growth deceleration was broad based with declines observed in 73% of Indeed’s occupational sectors. At its current pace of deceleration, the Indeed posted wage growth would approach 3.5% next month and is on track to return to 3.1% (average growth in 2019) in April 2024. Historically, this alternative index has been a leading indicator to the widely followed Atlanta Fed’s Wage Growth Tracker.

2) Energy Sector Gaining Relative Strength

Since the higher than expected January CPI print, the the energy sector is regaining strength relative to broader market (blue) while the technology sector weakens (orange). Energy is best-performing sector and technology is the worst-performing sector since the CPI report. This comes after Nvidia’s market capitalization has now eclipsed the entire S&P 500 Energy Sector. Interestingly enough, as of Friday’s close, the closely watched Cleveland Fed NowCast has February headline CPI inflation data moving higher with MoM projections coming in at 0.42%, or annualized headline inflation over 5% to levels not seen since September 2023.

https://www.clevelandfed.org/indicators-and-data/inflation-nowcasting

3) Used EV & Lithium Price Declines

Slumping EV prices due to price cuts and lowered demand have now caused leasing companies to demand concessions from EV makers, including agreements that manufacturers will buy back vehicles, to protect against further price erosion in the $1.2 trillion used car market. Tesla’s Model 3 and Audi’s e-Tron EV models have seen the biggest YoY price declines according to AutoTrader data. Meanwhile,prices of lithium, a key input into EV batteries, are down as much as 90% since the start of last year, while the price of nickel has roughly halved causing many companies to suspend new mining projects.

Stocks I’m Watching

Honorable mentions that didn’t make the final cut: SM, CSX, AER, GS, MMC, BMI, EWC, GEHC, MAX, BXSL, FTI, TOL, PEB, JHG, ALLY, INCO, FLS, HST, MTDR, COP, TPH, HTGC, CNQ, NOG, PSCE, CMPR, SU, OVV, INFY, SNPS, NDSN, IQV, CASY, CNI, DY, OWL, MPWR, UNP, H, QTWO, BX, BLK, WIT, MELI, CAN, ZTS, PBPB, RBA, TPX, MORN, JEF, EQH, WTTR, AOS, OTIS, BNRE, IDXX, AVY, LNW, EGLE, SBLK, GOGL, REVG, AMEH, UFPT, NUE, STLD, CLBT, SQSP, BLBD, WRB, LPLA, ERJ, TXT, VRNS, CELH

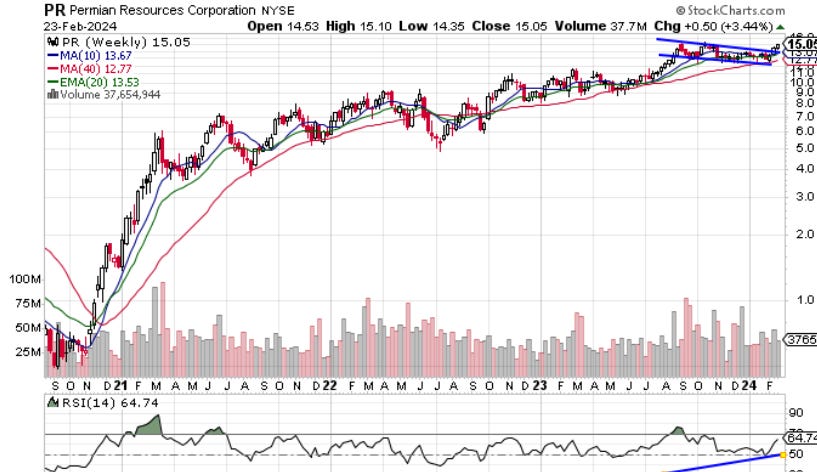

1) Permian Resources Corporation (PR)

Permian Resources Corporation, an independent oil and natural gas company, focuses on the development of crude oil and related liquids-rich natural gas reserves in the United States.

The U.S. oil and gas sector consolidation and M&A binge continued last week with Chord Energy (CHRD) announcement to purchase Enerplus (ERF) for $11B which follows Diamondback Energy’s (FANG) recent $26B purchase of Endeavor Energy Partners. Attention has now shifted to smaller Permian players such as Permian Resources (PR), SM Energy (SM), and Matador Resources (MTDR). Permian Resources is the second largest Permian Basin pure-play E&P while sporting FY24 EPS and free cash flow growth estimates of 62% and 96%, respectively, and a free cash flow yield of 15% trading at forward P/E of 7X. Last December, TD Cowen noted that Permian Resources sported attractive assets for a potential sale to the likes of larger E&P companies such ConocoPhillips, Occidental Petroleum and Devon Energy. Regardless, deep pocketed larger E&P names are hungry to acquire acreage and on the prowl for attractive assets. From a technical perspective, Permian is breaking out a weekly bull flag and has seen buyers step in at its rising 40WK moving average. Earning are expected 2/27 AH.

2) Coty Inc (COTY)

Coty Inc., together with its subsidiaries, manufactures, markets, distributes, and sells beauty products worldwide. It operates through Prestige and Consumer Beauty segments. Coty is one of the world’s largest beauty companies with a portfolio of iconic brands across fragrance, color cosmetics, and skin and body care.

Investors, particularly TD Cowen, seemed to like what they heard from Coty CEO Sue Nabi during last Tuesday’s 2024 Consumer Analyst Group of New York Conference as TD Cowen issued an upgrade to “Outperform”. Coty provided an FY24 outlook of revenue growth of +9% to +11% and adjusted EBITDA growth of +11% to 12%, implying margin expansion of +10 to +30 basis points while talking up its e-commerce growth, stellar performance of Burberry Goddess fragrance, and growth opportunities to expand in Latin America, China, and the Asia Pacific. Perhaps most importantly, Coty discussed how they are on track to continue deleveraging their balance sheet and are on track to reduce leverage towards 2.5x exiting calendar year '24 with leverage of around 2x exiting calendar year 2025 and beyond. Earnings estimates call for EPS growth of 25% and 20% in 2025 and 2026, respectively while trading at a discount to industry peers. From a technical perspective, Coty had a weekly breakout last week on strong volume as key moving averages appear to be inflecting higher after reporting another strong earnings report and analyst upgrades.

3) Summit Materials (SUM)

Summit Materials, Inc. operates as a vertically integrated construction materials company in the United States and Canada.

Lost among the noise of Nvidia’s much anticipated earnings release last week was the materials sector (XLB) having a weekly breakout. Summit Materials, an XLB index component, has seen strong accumulation volume come in ever since the second week of January 2024 on the right side of its weekly base and received an “Overweight” JP Morgan analyst upgrade last week from JP Morgan citing an improved profit outlook. Other XLB components and peers such as Vulcan Materials (VMC) and Martin Marietta (MLM) are already in strong uptrends. Summit is expected to host an investor day on March 13th. Consensus estimates call for free cash flow growth of 94%, 24%, and 38%, from FY2023-FY2025, respectively, while sporting forward P/E of 14X. From a technical perspective, key moving averages are inflecting higher as Summit looks for a follow through move after its weekly breakout.

Disclaimer:

All investment strategies and investments involve risk of loss. Nothing contained in this website should be construed as investment advice. Any reference to an investment's past or potential performance is not, and should not be construed as, a recommendation or as a guarantee of any specific outcome or profit.