Weekly Stock Bullfinder - Week of 2/5

Weekly Stock Bullfinder - Week of 2/5

Stocks I'm Watching - Week of 2/5

Hope everyone had a nice weekend!

Data Center Value Chain- Investment in Data Center Infrastructure Continues

Data center infrastructure build outs continue to boom in order to support both emerging cloud and artificial intelligence technologies as well as to address privacy and geopolitical risks. In my newsletter for the week of 1/22 titled “Semiconductor Arms Race- Wall St. Analysts Still Playing Catch Up”, I alluded to the significant earnings estimates re-rating in companies such as Super Micro Computer, NVIDIA, and semiconductor capital equipment names such as Applied Materials after Taiwan Semiconductors' bullish capital expenditure forecast. However, when digging into the the data center value chain, there exists a wide breadth of other names who are also benefiting from the expansion of data centers and the retooling of existing data centers needed to support emerging artificial intelligence technologies and service offerings.

Credit: @EricFlaningam

At its core, data centers are a combination of infrastructure and real estate with power (electricity) being one of the largest expenses to operators. According to IEA estimates, data center power consumption in the US is set to reach 35GW by the end of the decade, almost double its 2022 level, and by 2030, forecasts suggest that data centers alone could draw up to 21% of the world’s electricity supply. Power demands for data centers are driven by graphics processing units (GPUs) and related servers, which are power-hungry hardware, used to train increasingly sophisticated and complex artificial intelligence technologies. As a result, the exponential forecasted growth of artificial intelligence technologies is not just a story of who has the latest and greatest GPU hardware chip, but is rather increasingly fundamentally becoming an infrastructure story of power supplies, electrical, and cooling technologies in which many existing data centers simply cannot accommodate.

My point is while NVIDIA and Super Micro Computer, and cloud service providers bask in the business news media AI limelight, its important to note that the data center retrofit and expansion is not simply a semiconductor sector only thematic. For example, industrial suppliers such as Vertiv Holdings (VRT), Eaton (ETN), Comfort Systems (FIX), nVent Electric (NVT), Hubbell Incorporated (HUBB), Atkore (ATKR), among others, are strongly benefitting from supporting the “guts” of the data center retrofits and build outs as they support the ever increasing power and cooling demands of artificial intelligence deployment. In addition, infrastructure players such as MYR Group (MYRG), Emcor Group (EME), and Quanta Services (PWR) are benefiting from the related electrical grid upgrades needed for transmission to and from data centers locations. To this point, seeing the growth potential and importance of data center infrastructure, large private equity players have now emerged onto the scene plopping down significant investments into data center infrastructure throughout the world. In fact, in 2022, private-equity firms accounted for over 90% of an estimated $48 billion in global data-center mergers and acquisitions. For example, Blackstone (BX), the world’s largest private equity firm, completed a $10B takeover of data center operator QTS in 2021 and has become North America’s largest provider of leased data center capacity based on megawatts under contract. In addition, in May 2022, KKR joined investment firm Global Infrastructure Partners in a $15 billion deal to acquire CyrusOne, which operates more than 50 data centers across North America, South America and Europe. Asia is also becoming the latest hunting ground for global investors KKR to Bain Capital in data centers, as bets are placed on the region’s growing computing needs. Bain Capital announced a deal last August to take Beijing-based data center business Chindata Group Holdings private with an implied equity value of $3.2 billion. Finally, last September, KKR & Co. agreed to acquire a 20% stake in Singapore Telecommunications Ltd.’s regional data center business for about $800 million and sees the potential to invest $1 billion in equity on data center projects in the Asia-Pacific region in coming years.

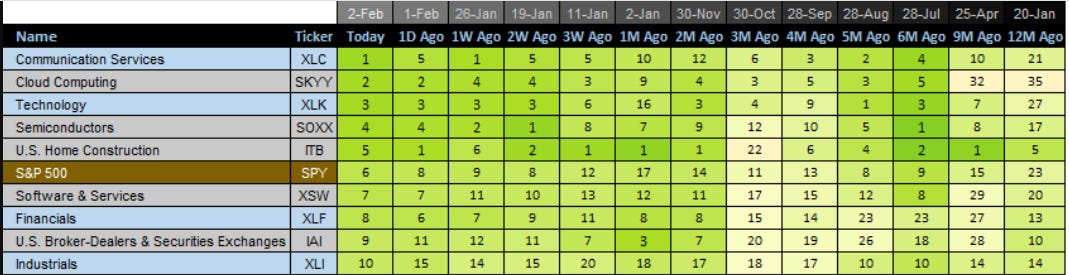

Relative Strength Update

Industrials (XLI) showed a 10 spot jump higher from 3 weeks ago while the communication services (XLC) sector takes the leading position after a strong earnings report from Meta Platforms (META) last week. Meta Platforms shares exploded 20% higher in Friday's trading as the company added $204.5 billion to its valuation. That made for the largest one-day market-cap haul in Wall Street history, surpassing the $191.3 billion one-day gain that Amazon.com Inc. (AMZN) had back in February 2022. Meta Platforms CEO Mark Zuckerberg stands to receive a payout of ~$700 million a year from Meta's first ever dividend which was announced on Friday.

Quotes of the Week

1) “I recently shared that, by the end of this year, we'll have about 350,000 H100s, and including other GPUs, that will be around 600,000 H100 equivalents of compute. We're well positioned now because of the lessons that we learned from Reels. We initially underbuilt our GPU clusters for Reels. And when we were going through that, I decided that we should build enough capacity to support both Reels and another Reels-sized AI service that we expected to emerge, so we wouldn't be in that situation again. And at the time, the decision was somewhat controversial, and we faced a lot of questions about CapEx spending, but I'm really glad that we did this. Now going forward, we think that training and operating future models will be even more compute-intensive. We don't have a clear expectation for exactly how much this will be yet, but the trend has been that state-of-the-art large language models have been trained on roughly 10x the amount of compute each year. And our training clusters are only part of our overall infrastructure, and the rest, obviously, isn't growing as quickly. But overall, we're playing to win here, and I expect us to continue investing aggressively in this area. In order to build the most advanced clusters, we're also designing novel data centers and designing our own custom silicons specialized for our workloads.”

-Mark Zuckerberg, Founder, Chairman & CEO Meta Platforms (META)

2) “So if you just look at our -- some of our consumer businesses, on the retail side, we built a generative AI application that allowed customers to look at summary of customer review, so that they didn't have to read hundreds and sometimes thousands of reviews to get a sense for what people like or dislike about a product. We launched a generative AI application that allows customers to quickly be able to predict what kind of fit they'd have for different apparel items. We built a generative AI application that in our fulfillment centers, that forecasts how much inventory we need in each particular fulfillment center. And so the start of the rollout of Rufus today is really just another step, but we think one that's pretty meaningful in being a generative AI powered shopping assistant and it's trained on our very expansive product catalog as well as our community Q&A and customer reviews and the broader web. But it lets customers discover items in a very different way than they have been able to on e-commerce websites. So if you want buying advice, like what should I look for in a pair of headphones or if you are doing purpose buying, like what should I buy for cold weather golf or comparisons, what's difference in lip-gloss or lip oil or you want recommendations of the best Valentine's Day gifts or you're on a detailed page with bridge product info, where you don't want to go through the whole page, you want to ask is this pickle ball rack that's good for beginners. All those questions you can pull in and get really good answers. And then it's seamlessly integrated in the Amazon experience that customers are used to and love to be able to take action. So I think that that's just the next iteration. I think it's going to meaningfully change what discovery looks like for our shopping experience and for our customers.”

-Andrew Jassy, President & CEO Amazon.com (AMZN)

3) “So, I think the bottom line is, we've got a $2 trillion deficit. 92% of the world's countries have deficits. There is going to be an enormous demand for money. Number two, we are the only significant democratic country that doesn't have any kind of national sales tax. We have some flexibility. However, you have to look at every time there's been a need to come to a conclusion, Democrat or Republican, the conclusion has been both parties spend more money. So what that tells you is spending money and not having taxes go up are a cornerstone of the policies both parties have chosen to follow. At some point, we're going to have to decide someone is going to have to pay for all we're doing. And whether that's a value-added tax or increasing income taxes or whatever, we are going to have to do something, and it's going to happen during the next presidential period, or Social Security and Medicare, Medicaid are going to be in jeopardy. So I don't think it matters who's elected. That's a problem that we're going to face. It won't happen till after the election. Whomever is elected won't matter. And I think that's going to mean is we're going to have some pressure on inflation, pressure on government spending, and I don't think that means good things for interest rates coming down. I would expect interest rates at best will be flat. I think people are biased by the fact that we had an extended period with extraordinarily low interest rates. I don't think interest rates are going to go crazy, but I don't think we're going to see them consequentially lower than they are now and probably a little higher.”

-Bill Berkley, Executive Chairman W. R. Berkley Corporation (WRB)

Some interesting charts from this past week:

1) Commercial Real Estate Pain Returns

US commercial real estate woes returned to the market headlines last week as New York Community Bancorp’s decisions to both slash its dividend and stockpile credit loss reserves ($552M increase, primarily due to its office exposure) sent its stock down a record 38% on Wednesday. In addition, Tokyo-based Aozora plunged more than 20% after warning of US commercial-property losses, and Frankfurt’s Deutsche Bank AG more than quadrupled its US real estate loss provisions. According to commercial real estate provider Trepp, banks are facing roughly $560 billion in commercial real estate maturities by the end of 2025, representing more than half of the total property debt coming due over that period. Over the past year, US commercial real estate property values have continued their valuation decline led by office (-25%), apartments (-12%), self-storage properties (-11%), and industrial (-1%).

2) Super Bowl Tickets Prices Surging

Tickets to next week’s Super Bowl football game in Las Vegas, NV between the Kansas City Chiefs and San Francisco 49ers are the most expensive ever for the event, going for an average of $9,815/each. The price is 70% more than the average of last year’s game and 40% above the previous record set in 2021.

3) Cloud Businesses Still Humming- Three Horse Juggernaut

Cloud computing services provided by Microsoft, Google, and Amazon continue to accelerate at a rapid pace with all companies sporting a CAGR of ~25% or higher over the most recent four year period. Amazon’s Web Services cloud services continues to be the cloud market share leader (31% market share), but Microsoft Azure’s cloud service is growing faster over the latest quarters and now has a cloud market share of 28%. Cloud services continues to generate massive free cash flow at scale for both Amazon (30% op margin) and Microsoft (50% op margin) while Google Cloud is quickly playing catch up. Since 2020, Google Cloud operating margins have improved from -62% in Q1 2020 to +9.4% in Q4 2023 while cloud revenues have tripled to an annualized run rate of now over $36.8B.

Stocks I’m Watching

Honorable mentions that didn’t make the final cut: FDS, WCC, GS, NU, CARR, CSX, EQIX, H, FROG, METC, MSCI, HUBB, WWD, GIC, SNA, VMC, CVLT, AVTR, GGG, SYK, MFC, RNR, EAT, CP, EU, AXP, AME, TREX, BLBD, CX, ENSG, LPLA, FCU.TO, AAOI, DCI, MDB, PLAY, JHG, ARCB, XP, AMAT, SNAP, SNOW, TCS.IN, FLEX, CPRT, AME, MCO, WSC, DNN, NXE, INOD, DSP

1) Encore Wire (WIRE)

Encore Wire Corporation engages in manufacture and sale of electrical building wires and cables in the United States. It sells its products to wholesale electrical distributors primarily through independent manufacturers’ representatives for residential, commercial, industrial, and renewable energy sectors.

Encore Wire is a pure play in the manufacturing of copper wire who has 24% short float while sporting $0 debt at 9X forward P/E and and continues to aggressively buyback shares (11% reduction over past year). As discussed earlier, an emerging thematic continues to be a heavy focus on infrastructure stimulus combined with data center nearshoring and upgrades, all of which benefit names like Encore. Last quarter, Encore noted that “their [distributor customers] destocking programs are either complete or very close to complete” and talked up big orders from data center AI upgrades or expansions as well as its new XLPE or cross-link products. Encore is also levered to construction spending which has been surprised or been revised up the past two months (December construction spending +0.9% month/month vs. +0.5% est. & +0.9% in prior month (revision up from +0.4%)). In addition, construction spending just hit new all-time highs of $2.09T, up +13.9% YoY. Finally, other electrification and infrastructure beneficiaries such as Powell Industries (POWL) have had post-earnings rippers and Encore’s high short interest could result in a squeeze if earnings surprise. From a technical perspective, Encore is emerging from a weekly bull flag riding its 10WK moving average to higher prices. Earnings expected 2/14.

2) Piper Sandler Companies (PIPR)

Piper Sandler Companies operates as an investment bank and institutional securities firm that serves corporations, private equity groups, public entities, non-profit entities, and institutional investors in the United States and internationally. It offers investment banking and institutional sales, trading, and research services for various equity and fixed income product

Piper Sandler had a weekly breakout last week on strong volume after announcing a strong earnings report which featured it’s advisory services generating $284 million of revenues during the fourth quarter, nearly double the sequential quarter and up year-over-year while it repaid $125 million of senior notes procured for the acquisition of Sandler O'Neill. Piper also announced a $1/share special cash dividend (paid on March 15 to shareholders of record as of the close of business on March 4). Piper continues its leadership position as the #1 adviser in U.S. bank M&A based on the number of announced transactions and the aggregate deal value and they advised on seven of the largest 10 bank mergers and acquisitions completed during 2023. Expecting a continued rebound in capital markets activity, consensus EPS estimates call for growth of 27% and 30% in 2024 and 2025, respectively.

3) Old Dominion Freight Line (ODFL)

Old Dominion Freight Line, Inc. operates as a less-than-truckload (LTL) motor carrier in the United States and North America. It provides regional, inter-regional, and national LTL services, including expedited transportation.

Old Dominion beat earnings estimates last week and raised its quarterly dividend by 30% as it consistently absorbs economic headwinds in industrial demand with its strong pricing power. Perhaps transports are sniffing out a potential bottoming in ISM manufacturing activity as ISM Manufacturing new orders last month turned up sharply reaching its highest level in 17 months. Peers SAIA, XPO, TFII and other transports like railroads have seen strong volume pour in as the IYT transports ETF approaches its weekly breakout level. Old Dominion Freight Line has been an institutional favorite and a standout portfolio performer over the past decade, consistently gaining market share and returning over 1,000%. From a technical perspective, Old Dominion is forming a weekly bull flag and has consistently seen buyers step in at its rising 40WK moving average.

Disclaimer:

All investment strategies and investments involve risk of loss. Nothing contained in this website should be construed as investment advice. Any reference to an investment's past or potential performance is not, and should not be construed as, a recommendation or as a guarantee of any specific outcome or profit.