Weekly Stock Bullfinder - Week of 3/11

Weekly Stock Bullfinder - Week of 3/11

Stocks I'm Watching - Week of 3/11

Hope everyone had a nice weekend!

Google Search- Searching For Answers in the New AI Landscape?

Over the past month month, Alphabet’s botched rollout of the Gemini large language model (LLM) has given rise to significant media chatter that Alphabet is falling behind in artificial intelligence innovation and its “bread and butter” internet search product is under an imminent disruption threat from emerging competitors such as Chat GPT, Claude, Grok, Llama 2, and others. Stating the obvious, the Gemini LLM rollout has been a black eye to Google’s leadership and has been seized upon by competitors to imply Google is simply not innovating and moving fast enough to address new AI chatbot and LLM threats to its search business. These questions are fair to ask; after all, search advertising revenue made up the majority—or 59%—of Alphabet’s total revenues last year. However, there are a number of reasons that the chatter around Alphabet’s quick demise may be misplaced, offering a potential opportunity down the line if price continues to correct (now 12% lower than its recent 52 week high).

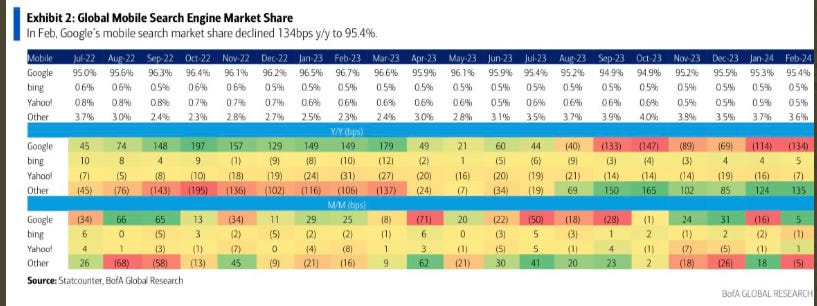

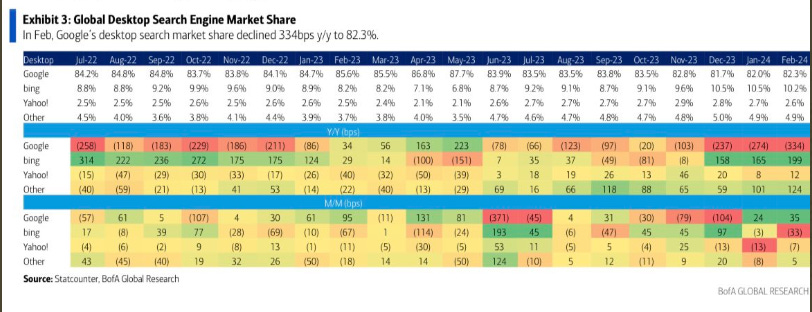

1) Google Search Market Share Shows No Signs of Readily Apparent Cracks

Ever since the release of Google Search in 1997, the company's search engine has dominated the search engine market, maintaining a commanding market share of more than 93% since January 2015. Well, where are we now? Looking at the Statcounter and Bank of America Global Research data through February, Google search continues to have a ~95% global mobile search market share and an ~82% global desktop search market share. Both search market shares have roughly hovered within 200-300 bps since July 2022. In addition, recent entrants such as Bing and ChatGPT global downloads remain choppy at best; Bing and ChatGPT global downloads were down 57% and 15%, month over month, respectively.

2) Enterprise AI LLM Adoption Appears Restricted To Company Data

Gartner Group predicts that by 2026, over 80% of enterprises will be using generative AI, including the deployment of generative AI enabled applications in their production environments. Recent earnings calls from Dell, Pure Storage, NetApp, Broadcom, and C3AI continues to suggest that LLM AI enterprise deployments are focused on customer tailored LLM’s being trained and implemented on localized company data. Open Source LLM’s are not being widely implemented at the enterprise level due to due to emerging research from University of Carnegie Mellon, which has highlighted cyber-attack opportunities exposed by open source large language models, as well as Korean electronics giant Samsung’s embarrassing leak of proprietary source code software used for measuring semiconductor equipment to ChapGPT.

3) Google Search Has Evolved Before and Has the Free Cash Flow to Adapt Accordingly

In a recent MS Technology conference last week, Philipp Schindler, Senior Vice President and Chief Business Officer of Google, highlighted Google’s search product has evolved before from similar perceived threats such as the introduction of mobile apps, social media search, and e-commerce sites. Despite all of this, Google has seen positive search query growth in all of their major markets over the past 12 months and 80% of all of Google’s advertisers are now using at least one AI-powered search solution today. Schindler also talked up how generative AI searches could see embedded advertising and emerging generative AI opportunities moving forward which Google has deep mastery and expertise implementing.

MS Conference Transcript

https://abc.xyz/philipp-schindler-senior-vice-president-and-chief-business-officer-of-google-at-the-morgan-stanley-technology-media-and-telecom-conference-on-march-6th-2024/

Taking It All Away

1) While Google’s Gemini LLM launch was a disaster and black eye for CEO Sundar Pichai, media attention suggesting an imminent demise of Google’s search business appears unfounded in the actual real time market data (even after the rollout of ChatGPT and other chatbots). In addition, former Google co-founders Sergey Brin and Larry Page appear to be re-engaged to push Google’s AI efforts and current CEO Sundar Pichai may be under additional pressure moving forward to quickly bounce back and clean up the botched Gemini rollout.

2) Forward looking, Google will need to step up their game to keep up with the competition and defend its search business from new open source chatbots and LLM’s such as ChatGPT, Perplexity, Llama 2, etc. Many important legal questions remain to be solved surrounding LLM AI “training data” which could be sourced from copyrighted or paywalled text and image materials. Many LLM’s do not attribute their source today which could be ripe for legal challenge. For Google, a treasure trove of training data from its core search products to other products such as G-Mail, Google Maps, YouTube, and others remains at its disposal, providing it a clear strategic advantage. In addition, there remains significant questions for LLM’s around their long term economics to offset the tremendous capex cost (chip hardware, energy, etc.) of continually training and maintaining LLM’s (many of which do not have an embedded advertising component, something that Google has deep mastery in which its existing advertising platforms). In addition, Google already has its own proprietary chip hardware, tensor processing units (TPUs), for AI training and inferencing, lessening its reliance on fabless chip designers such as Nvidia and AMD.

3) While Google search takes the brunt of the media heat, several other Google businesses such as Android, YouTube, Waymo, Cloud, and others continue to hum along building out Alphabet’s diverse empire. YouTube is averaging 70 billion in daily views which is included within Google’s now $15 billion annual subscription businesses. Just last week, Waymo was approved by the California Public Utilities Commission (CPUC) to expand its fared robotaxi services in Los Angeles, the San Francisco Peninsula, and on San Francisco freeways, and will begin testing its vehicles in Austin, Texas ahead of launching its ride-hailing services in the city.

4) In the past, big tech “scandals” such as Meta’s Cambridge Analytica and Russian targeting/meddling, Meta’s capex spending foray into developing the metaverse, to Google’s flirtations with China to develop a censored search platform, have all afforded tremendous buying opportunities for the savvy long term investor. This is partially because Big Tech companies produce tremendous amounts of free cash flow from their core businesses allowing for temporary slips and wobbles when they strike out or simply get into trouble (legal, EU fines, etc.). While Google’s current 12% pullback is extremely minor, further selling pressure down to its rising 200WK moving average or ~16% lower from current levels (an area of support from its Covid-19 March 2020 panic low and recent October 2023 market correction low) could offer a compelling opportunity.

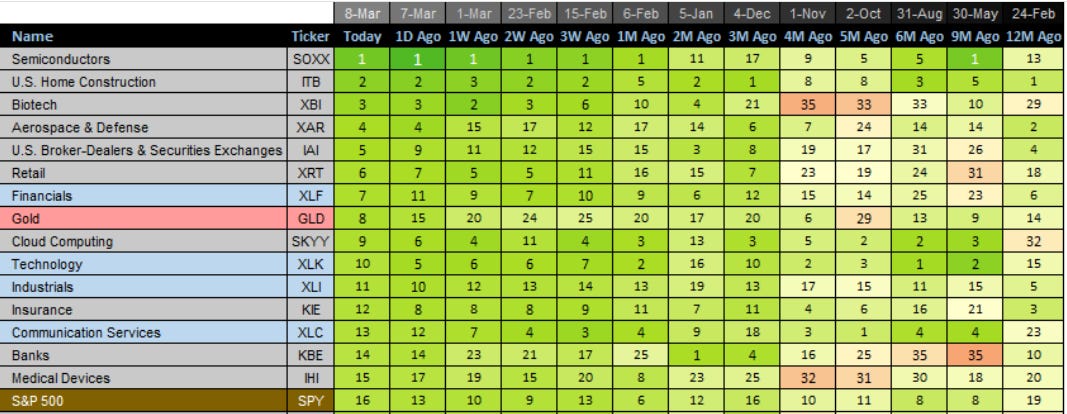

Relative Strength Update

Gold surges up 17 spots from 3 weeks ago while other notable group moves include Aerospace and Defense (XAR- up 8 spots), Brokers and Dealers (IAI- up 10 spots), and retail (XRT- up 5 spots). Semiconductors (SOXX) and Home Construction (ITB) continue holding up strong in the top two market leadership groups.

Quotes of the Week

1) “A couple of comments about inflation. In the last quarter, in the first quarter, we estimated that year-over-year inflation was approximately zero to 1%. We'll now say that in Q2, it was essentially flat. And notwithstanding essentially flat, we're taking price reductions where we can. Anecdotally, everything from simple items like reading glasses from $18.99 to $16.99, the 48 count of Kirkland Signature batteries from $17.99 to $15.99, a 24 count of Pellegrino from $16.99 to $14.99, and even a four pounds of frozen three berry fruit blend from $14.99 down to $10.99 with new crop pricing. So, we continue to do that. We always want to be the first out there trying to lower prices. Many new items in sporting goods and lawn and garden are being set with lower prices year-over-year, and overall, mostly due to reduced freight costs and lower commodity costs versus a year ago. And overall, our inventories and SKUs are in good shape across all channels. Overall, we've had good seasonal sell-through during the quarter. In terms of shipping and supply chain issues, we've been asked about that often of late. There are some delays, generally just a couple to three weeks, but mostly now planned for. First, there was an issue a while back with the Panama Canal challenges. Then, of course, the Red Sea challenges. A lot of that has to do with changing the way ships are being routed. No meaningful pricing issues because a lot have been placed contracts.”

-Richard Galanti, CFO Costco Wholesale Corporation (COST)

2) “The current macro environment remains stable and consistent with prior quarters. We expect continued deal scrutiny throughout this coming year. We remain focused on operational excellence, while delivering market-leading growth at scale, assisting organizations of all sizes to consolidate and improve their cybersecurity. In contrast to the macroeconomic backdrop, the state of the threat landscape has never been more elevated. In CrowdStrike's recent 2024 Global Threat Report, we unpack the harsh realities of cyber today. Key findings include: first, attacks are faster than ever. What took adversaries hours has shrunk to minutes and seconds. Attack speeds will only accelerate. Second, the cloud is increasingly under attack. We tracked a 75% increase in cloud intrusion attempts. The cloud is today's battleground for cyberattacks. And third, generative AI is an adversary force multiplier. GenAI puts advanced cybercrime tradecraft in the hands of attackers of all skill levels, Gen.AI will dramatically grow the adversary population.”

-George Kurtz, CEO & Co-Founder, CrowdStrike Holdings (CRWD)

3) “I'm hearing this [returning to in-house data centers] in the marketplace and even my engineers have talked about it. Okay, that it's going to be cost effective for us to build. Now, the constraint is that you'd think, well, somebody needs to call up Jensen [Nvidia CEO] and beg for GPUs. Let's say we can figure out how to do that. Maybe we know somebody who knows Jensen. Okay, the hard part is we can't get power. So I think the constraint on this going for everybody sees with the constraint is availability of GPUs. I think it's straight on this soon is going to be the availability of power. You cannot get power to build the data center in Silicon Valley. You know this, right? Northern Silicon Valley is PG&E, which is, I have no comment on that. And Southern Silicon Valley is some other power company….they will not give you power for a data center. So I think this GPU constraint is ephemeral as soon as it's going to be power.”

-Thomas Siebel, CEO C3.AI (AI)

Some interesting charts from this past week:

1) Mortgage Rate Lock In Effect Easing?

New home listings are showing signs of perking up so far in 2024. In February 2024, there were 339,370 new US home sale listings, representing an 11% increase compared to February 2023 (304,868 new listings). However, this is still 17% below February 2019 levels (409,934 new listings). Redfin has reported new listings rose 13% from a year earlier nationwide during the four weeks ending March 3, the biggest increase in nearly three years. The boost in new listings helped bring the total number of homes for sale up 1.7%. Following eight months of declines, February is the first month the number of homes for sale has increased on an annual basis. Redfin reported asking prices of new listings posted their smallest increase in roughly two months; additionally, 5.5% of home sellers dropped their asking price, on average, the highest share of any February since at least 2015.

2) MSCI China ETF Total Returns

Over the last 30 years, the MSCI China index has posted a total return of 0%. This total return has been accompanied by 22 intra-year corrections of -20% (vs. 6 for the S&P 500) and an average annual correction of -30% (2x the S&P 500).

3) New US Semiconductor Manufacturing Projects

The map below illustrates the semiconductor manufacturing projects slated for completion between 2024 and 2028 across the US, driven by incentives from the Chips Act passed in July 2022. Samsung, Micron, Intel, and Texas Instruments, are initiating significant manufacturing expansions, each exceeding $1B, with Samsung establishing 11 new projects alone in Texas.

Stocks I’m Watching

Honorable mentions that didn’t make the final cut: RRR, ERJ, CTSH, LPX, HRB, APAM, MSM, QRVO, PKG, MPWR, DFH, FLS, POOL, MCHP, NXPI, FLS, ADI, AOS, TROX, MGY, VLO, IWO, AER, XLB, ATKR, SCCO, HTGC, SF, SQSP, AFRM, PIPR, ARCB, FANG, TDW, FTI, SQ, ALLY, TALK, STLD, EOLS, MNMD, CMPS, GOGL, SBLK, IOT, CL, ATAI

1) Carrier Global (CARR)

Carrier Global Corporation provides heating, ventilating, and air conditioning (HVAC), refrigeration, fire, security, and building automation technologies in the United States, Europe, the Asia Pacific, and international.

Carrier continues to divest non-core businesses to narrow its scope as a pure play heating and cooling equipment provider and made news last week when it announced the sale of its Industrial Fire business to Sentinel Capital Partners. Carrier expects net sale proceeds to exceed $1.1B and plans to use the proceeds to pay down debt and anticipates resuming stock buybacks, as it returns to ~2x net leverage by year-end 2024. This follows Carrier’s other deal announcements to sell its Global Access Solutions business to Honeywell for nearly $5B and its Commercial Refrigeration business to Haier for $775M. At the recent Barclays Industrial Conference, Carrier pointed to a strong start to 2024 with orders from US and European markets as well as seeing benefits from secular growth pockets such as data center cooling and K-12 HVAC upgrades. From a technical perspective, Carrier attempted to breakout last week from its weekly base on high volume but was held back by a weak market. Look for follow through move through the $58 resistance level.

2) Q2 Holdings, Inc (QTWO)

Q2 Holdings, Inc. provides cloud-based digital solutions to regional and community financial institutions in the United States. The company offers Digital Banking Platform, an end-to-end digital banking platform supports its financial institution customers in their delivery of unified digital banking services across digital channels.

Q2 Holdings continues to make technology inroads with serving financial institutions of all sizes including Tier 1 banks, credit unions, and small to medium sized banks. All top 10 US credit unions utilize Q2 Holdings retail solution and Q2 Holdings had record bookings in its most recent fourth quarter. Backlog increased by $269.2 million sequentially, resulting in backlog of approximately $1.8 billion as of Q2 Holdings quarter-end, representing 17% sequential growth and 23% year-over-year growth. Q2 holdings is GAAP profitable, has long term subscription contracts averaging 66 months, is currently trading at forward P/E of 38X, and has EPS growth estimates of 55%, 34%, and 32% from 2024-2026, respectively. Free cash flow is expected to grow to $101M in 2025, an increase of 56%. From a technical perspective, Q2 Holdings is flashing signs of bottoming after its most recent earning report as key moving averages have inflected higher and price has cleared the $48 weekly base resistance level.

3) Pure Storage (PSTG)

Pure Storage, Inc., together with its subsidiaries, provides data storage technologies, products, and services in the United States and internationally.

Data storage providers NetApp (NTAP) and Pure Storage (PSTG) have both emerged as potential AI thematic winners this past earnings season with significant post-earnings gap ups from long weekly bases. As companies attempt to implement AI technologies using their localized data, both companies have stepped in to address two core AI implementation problems; 1) existing data storage arrays were selected to provide just enough performance for their primary function, leaving little performance left for AI access 2) existing storage arrays are not networked, limiting access to AI apps not provisioned directly on their primary compute stack. During its most recent earnings call, Pure Storage’s CEO expressed strong confidence in returning to double-digit revenue growth based on AI tailwinds and touted a notable eight-figure deal signed in the past quarter with a major graphics processing unit (GPU) cloud provider. Earnings estimates call for 199% and 47% EPS growth in FY25 and FY26, respectively. From a technical perspective, Pure Storage needs several weeks of consolidation to allow moving averages to catch up but could offer entry opportunity with pullback to its rising 10WK moving average.

Disclaimer:

All investment strategies and investments involve risk of loss. Nothing contained in this website should be construed as investment advice. Any reference to an investment's past or potential performance is not, and should not be construed as, a recommendation or as a guarantee of any specific outcome or profit.

Carrier looks good!!

Loved this write up on GOOG, PSTG etc.