Weekly Stock Bullfinder - Week of 3/18

Weekly Stock Bullfinder - Week of 3/18

Stocks I'm Watching - Week of 3/18

Hope everyone had a nice weekend!

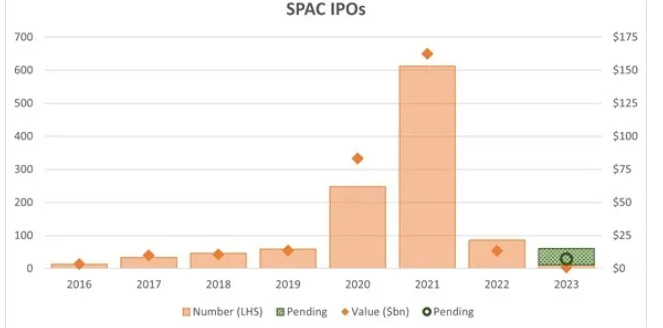

The SPAC “Scarlet Letter”

The COVID-19 pandemic period from 2020-2021 featured a capital markets mini-bubble in special purpose acquisition companies (SPACs) fueled by sponsors raising new IPOs with a relentless fervor while market participants were happy to oblige. SPACs were able to raise record proceeds in 2020 and 2021, with 2021 seeing SPAC IPO values eclipsing $600B in total. At their peak from 2020-2021, SPACs accounted for the majority of new U.S. public stock market listings, exceeding traditional IPOs. In the fever pitch of SPAC’s in 2021, SPAC’s accounted for almost a 60% share of new public stock market listings. Among other benefits, the large appeal of SPACs for sponsors and target companies was the looseness of disclosures and absence of transparency around future projections compared to traditional IPO’s. This led to SPAC’s including pie in the sky growth and earnings projections from numerous sectors such as electric vehicles and other green energy companies (think Nikola and Lordstown Motors, We-Work, etc.), among others, while the sponsors, which at its peak sometimes included celebrities and social media influencers, earned highly lucrative sponsor fees. Meanwhile, many SPAC’s overpromised and woefully under delivered compared to projections and most SPAC investors from this period have stomached abysmal market returns. The De-SPAC Index, which measures the performance of companies taken public through a SPAC merger, fell almost -75% in 2022, after losing -45% in 2021. Of the SPAC merger IPO’s in 2022, the average return after 1 year was -58%. As a result, many SPAC’s wear the “scarlet letter” and continue to be shunned from the vast majority of Wall St and institutional money manager portfolios.

“Lost in the sauce” of SPAC mania was select legitimate companies with strong fundamental growth prospects such as Draftkings (DKNG) and Sofi (SOFI), among others. Granted their sky high SPAC valuations needed some time to re-rate and digest themselves (i.e. Draftkings at one point traded at a stratospheric 33X (!) sales multiple in September 2020), these companies stand out as successes from the SPAC mania from 2020-2021. One company, Israel-based digital intelligence company Cellebrite (CLBT), went public with a SPAC called TWC Tech Holdings Corp II, and may be showing fresh signs, similar to Draftkings and Sofi, that it may also shake off the SPAC scarlet letter.

Just last week, Williar Blair upgraded Cellebrite to an “Outperform” rating ahead of its much anticipated first investor day upcoming on March 27th. In 2023, Cellebrite posted an impressive a string of earnings beats off the back of racking up impressive new contract wins and expansions with its various customers including U.S. federal customers, police departments, and commercial companies. Within digital forensic crime units, Cellebrite is widely recognized as the best-in-class leader for its digital forensic software that is used to access mobile phones, extract the data and reveal very important digital evidence for investigators. In addition, Celebrite’s Guardian and Pathfinder software solutions are used to advance cases involving digital evidence and apply machine learning and AI technologies to both surface leads and help investigators expedite their case investigations. Impressively, Cellebrite has achieved 20 straight consecutive quarters with its recurring net retention rate (NRR) above 120%, which supports the point that they rarely lose customers and are constantly upselling their new product capabilities and offerings to their installed “sticky” customer user base. Just last week, Cellebrite announced plans to achieve the highly important FedRAMP certification for their SaaS offering, a milestone they expect to achieve in the second quarter this year, which they believe will open up a significant amount of additional federal procurement opportunities and support large deployment of Cellebrite software at scale.

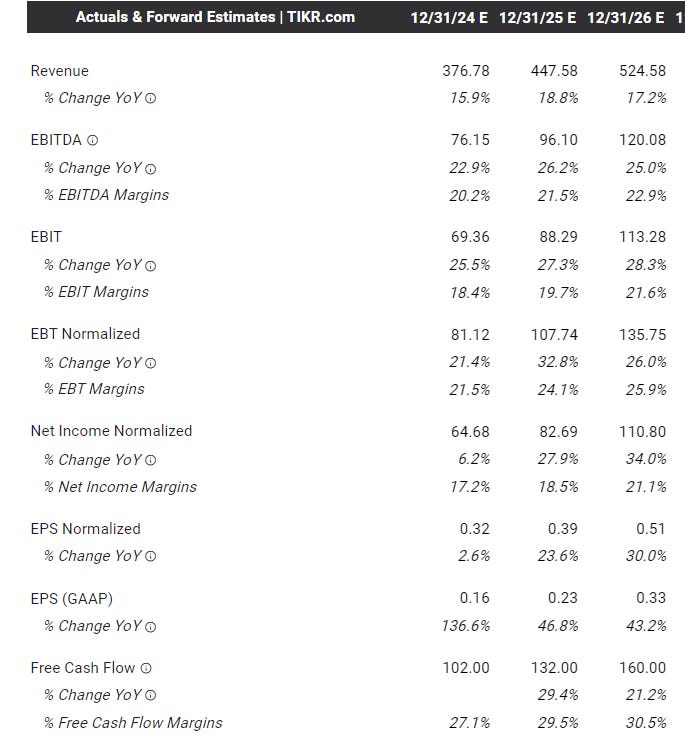

Moving forward, Cellebrite’s 2024 ARR target range guidance is from $380 million to $400 million or 20% to 27% increase over 2023, gross margins in the 82% to 84% range, and adjusted EBITDA in the range of $70 million to $80 million or 19% to 21% of total revenue. Cellebrite has minimal capital intensity expecting capital expenditures of just $8 million to $12 million in 2024 meanwhile it ended 2023 with cash, deposits and investments totaling approximately $332 million, an increase of 62% since the end of 2022, with no short term or long term debt on its balance sheet. Consensus free cash flow estimates call for growth of 29%, 30%, and 31%, from 2024-2026 respectively. With now 20 trading days over the $10 price level, this past week marked the first week since its SPAC IPO that its outstanding warrants are now callable. Cellebrite currently trades at 29X forward P/E and 5.3X sales.

From a technical perspective, Cellebrite is seeing support at its IPO weekly base breakout level as volume has substantially picked up since October which could be an indication some Wall St. funds and money managers may be warming up to this name and strong fundamentals. Cellebrite appears to have a strong niche moat and expanding customer base and could also make for an interesting M&A target from companies who support similar customers, such as Axon Enterprise (AXON), a company which currently dominates the hardware and software body cameras and tasers segment while supporting similar customers and sectors to Cellebrite.

Upcoming Cellebrite Investor Day Link:

https://onlinexperiences.com/scripts/Server.nxp?LASCmd=AI:4;F:QS!10100&ShowUUID=F90216BD-4299-4EFC-83D0-5BBA84DEE0A0

Quotes of the Week

1) “Let me add that Oracle has been building data centers at a record level and a lot of people I think are aware that we can build fairly small data centers to get started when we want to. But the unique thing about Oracle's data centers, they're all identical except for scale. We did not have custom data center. They all have all the Oracle services. They are all complete. One of the things that's unusual about them, they are all completely automated. They come up on their own and they kind of run themselves…..We can get a full cloud data center with Ultra services in 10 racks. But this is what I want to point out. We're also building the largest data centers in the world that we know of. We're building an AI data center in the United States where you could park eight Boeing 747s nose-to-tail in that one data center. So, we are building large numbers of data centers, and we were - and some of those data centers are smallish, but some of those data centers are the largest AI data centers in the world. So, we're bringing on enormous amounts of capacity over the next 24 months because the demand is so high, we need to do that to satisfy our existing set of customers. To give you an idea. One more thing, in terms of data centers we're building 20 data centers from Microsoft and Azure. They just ordered three more data centers this quarter. They're adding to that already.”

-Larry Ellison, Chairman and CTO, Oracle Corporation (ORCL)

2) “House of Sport is one of the most exciting concepts in retail today, and in 2024, we expect to open eight new locations. As we elevate our store portfolio, seven of these are planned relocations or conversions of existing DICK'S stores, along with one new store at Prudential Center in Boston. We expect to begin construction on approximately 15 House of Sport locations that are scheduled to open throughout 2025. We will also open 16 next-generation 50K DICK'S stores in 2024. As part of this, we will relocate or remodel 12 existing DICK'S stores into this innovative new format and open four new locations. Across our footprint, we will add approximately 50 premium full-service footwear decks, taking this elevated athlete experience to nearly 90% of our DICK'S locations… Before continuing, I want to share why we are so excited about these investments, especially the House of Sport and our next-generation 50K DICK'S locations. ….For a new House of Sport, in year one, we expect approximately $35 million in omnichannel sales and a very strong profitability with a target of approximately 20% EBITDA margins. In terms of capital, it will take about $11.5 million of net CapEx to open House of Sport location, resulting in an expected year-one cash-on-cash return of approximately 35%. We also expect attractive returns from our next-generation 50K DICK'S store investments, where we are targeting approximately $14 million in year-one omni-channel sales and a comparable EBITDA margin of approximately 20%.”

-Navdeep Gupta, CFO, Dicks Sporting Goods (DKS)

3) “Cisco Systems (CSCO) offers a good history lesson. I remember well the stock's behavior at a similar technology moment in time. In the three and a half years leading to March 9, 1994, CSCO soared ~31-fold from $0.07 to $2.24 split-adjusted, as its routers, switches, and other equipment dominated the buildout of the internet backbone globally. The capital markets began to fund competitors, even those with systems inferior to Cisco’s, which confused strategic planners in corporations and cast a short-term pall on spending. In the four months leading up to July 15, 1994, CSCO dropped 51% as companies—already worried about a potential recession—reassessed their spending commitments and deliberated. After the coast cleared, CSCO entered another ~73-fold run into the peak of the internet bubble during 2000. Today, Nvidia (NVDA) is that company. Central to the AI age, NVDA has soared ~117-fold in the roughly nine years since February 8, 2015, when analysts were beginning to understand that breakthroughs in Deep Learning were accelerating the pace of AI change, to the benefit of GPUs (graphic processing units). NVDA also had appreciated 23-fold in the five years since its last inventory correction, one triggered by crypto winter that hit it in October 2018 and trounced the stock by 56% in three months. The launch of ChatGPT in November of 2022 has fueled several quarters of unprecedented growth for Nvidia as cloud service providers, other consumer internet companies, and well-funded startups have scrambled—likely double- and triple-ordering GPUs in the process—to acquire Nvidia’s hardware and train AI models. Today, Nvidia is guiding expectations to a sequential deceleration in growth and, reportedly, the lead time for its GPUs has dropped from 8-11 months to 3-4 months, suggesting suggesting that supply is increasing relative to demand. Without an explosion in software revenue to justify the overbuilding of GPU capacity, we would not be surprised to see a pause in spending, compounding a correction in excess inventories, particularly among the cloud customers that account for more than half of Nvidia’s data center sales. Longer term, unlike the history with Cisco, competition could intensify, not only because AMD is finding success but also because Nvidia’s customers—cloud service providers and companies like Tesla—are designing their own AI chips.”

-Cathie Wood, Co-Founder and CEO Ark Invest

Some interesting charts from this past week:

1) Global Information Service Providers- Generative AI An Emerging Threat?

JP Morgan published research this past week on global information service providers who serve US consumer credit, legal information, financial market data and analytics, credit ratings, and index providers. JP Morgan Research noted that information services firms have meaningful barriers to entry from generative AI technologies as their core data sets are “behind a wall” or regulated data sets (i.e. consumer credit files) but noted it is watching generative AI impacts to legal services. They acknowledged many leading legal service providers already have a head start integrating generative AI technology into their core service offerings.

2) ESG- Losing Popularity on S&P 500 Earnings Calls

According to FactSet analysis of S&P 500 earnings calls, only 9 companies, led by the financials sector with 6 companies, cited “ESG” (Environmental, Social and Governance) during their earnings calls for the fourth quarter, below 5 & 10 year averages and the fewest mentions since 2Q 2019. Since peaking at 155 in 4Q 2021, companies citing “ESG” during their earnings calls have declined (Q/Q) in nine (9) of the past ten (10) quarters.

3) Semiconductor Sector TTM Economics

Below is a Goldman Sachs Global Investment Research chart showing semiconductor sector TTM non-GAAP gross margin and operating margins. Goldman points out that despite headwinds associated with product mix in the semiconductor business (i.e. increase in revenue derived from custom silicon vs. merchant silicon), Broadcom (AVGO) reported the the 2nd highest non-gaap gross margins (75%) and operating margins (57%) in FY1Q.

Stocks I’m Watching

Honorable mentions that didn’t make the final cut: INTR, NTAP, MU, STNG, TRMD, WWD, TPX, NPO, ASEA, WMS, WSO, CXT, L, MGY, FLS, TFII, ORCL, APP, ACMR, IMO, FROG, BWMN, LNW, DFH, MTDR, NOG, TOT.TO, VLO, CHRD, PBF, QSR, OXY, SXC, FCX, TROX, TECK, EQH, SYY, OWL, DBA, SU, WMB, ACTG, COP, STLD, FTAI, AER, CVI, WLK, TSCO, CI, OXY, PFG, ELV, LPLA, COF, PXD, CIVI, CRVL, STNE, ERJ

1) CVR Energy (CVI)

CVR Energy, Inc., together with its subsidiaries, engages in the petroleum refining and marketing, and nitrogen fertilizer manufacturing activities in the United States. It operates in two segments, Petroleum and Nitrogen Fertilizer.

CVR Energy is flashing signs of participating in the refining sector move (ETF “CRAK”) as industry peers such as Valero (VLO), Phillips (PSX), and Marathon Petroleum (MPC), have seen significant recent gains due to rapidly rising 3-2-1 Crack Spreads (which approximates the value of crude oil inputs and product outputs, in effect an indicator of refinery profitability). Since January 1st, 3-2-1 crack spreads have rebounded strongly by surging 41% higher, standing at $32.36 as of last Thursday. In addition, Ukraine continues to attack Russian refining facilities (Ukraine's drone strike campaign this year has hit facilities collectively accounting for 25 percent of Russia's total refining capacity of 6.8 million barrels per day) which may disrupt global products flows. CVR is a Carl Icahn favorite (Icahn holds about 66% of the outstanding shares (units) of CVR Energy) and has historically had shareholder friendly shareholder return policies. For example, for the full year of 2023, CVR authorized regular and special dividends of $4.50 per share for a total payout ratio of approximately 64% of free cash flow generated for the year. From a technical perspective, CVR had a weekly base breakout and could look for a follow through move if the rotation to energy names picks up steam this spring.

2) Ardmore Shipping (ASC)

Ardmore Shipping Corporation engages in the seaborne transportation of petroleum products and chemicals worldwide.

Due to continued Red Sea shipping disruptions, which many shipping industry experts agree are appearing more and more likely they will persist for the foreseeable future in 2024, product tanker MR spot earnings continue to hover well in excess of $40K and double the 5 year average from 2019-2023. Average product tanker earnings rose 28% week-over-week to $48,371/day amid surging LR markets in the East. Last quarter, Ardmore loosened the purse strings on its shareholder return program by increasing its dividend by 31% to $0.21/sh. From a valuation perspective, Ardmore sports a 5.5% dividend yield, 22% NTM free cash flow yield, and forward P/E of 5.8X. From a technical perspective, Ardmore has consolidated into a tight weekly cup and handle formation just below its weekly breakout resistance level. Continued spot pricing strength in the product tanker segment could lead to further analyst upgrades and a continuation breakout to new highs.

3) Devon Energy (DVN)

Devon Energy Corporation, an independent energy company, engages in the exploration, development, and production of oil, natural gas, and natural gas liquids in the United States.

Devon long held a reputation for operational excellence, and the stock consistently outperformed the XOP sector ETF from 2020 through late 2022 but has underperformed since late 2022, due to encountering a myriad of production and capex issues disappointing Wall St. Poor earnings results and guidance resulted in Devon undergoing a nasty 50%+ correction since the middle of 2022. However, Devon is flashing signs of a potential turnaround closing above its decline 40WK MA average with its 10WK threatening to cross above. With Permian oil and gas assets being scooped up left and right in M&A deals (since the beginning of last year, 8 of the 20 largest private Permian producers -- collectively responsible for more than 1 million barrels of production per day, have been acquired), and Devon already missing out on purchasing Enerplus and Marathon Oil, perhaps names such as EOG or COP would be interested in acquiring this turnaround play. At $85 average WTI prices, Devon’s free cash flow yield sensitivity analysis computes to approximately 13% while it is targeting a 70% cash returns (share repurchase, fixed dividend, and variable dividend) to shareholders in 2024.

Disclaimer:

All investment strategies and investments involve risk of loss. Nothing contained in this website should be construed as investment advice. Any reference to an investment's past or potential performance is not, and should not be construed as, a recommendation or as a guarantee of any specific outcome or profit.