Weekly Stock Bullfinder - Week of 3/4

Weekly Stock Bullfinder - Week of 3/4

Stocks I'm Watching - Week of 3/4

Hope everyone had a nice weekend!

Small But Interesting

To mix things up this week, below are some small cap names which I added to the tracking list this past earnings season based upon reviewing their earnings call results, investor presentations, and transcript.

QuickLogic Corp (QUIK)

QuickLogic is a fabless semiconductor company who operates an eFPGA IP solution, Australis, and an AI platform, QuickAI, specifically designed for endpoint AI applications development. Since launching in 2020, total revenue has grown 146% and fiscal 2023 saw Quicklogic hit an inflection point growing revenues 31% and achieving full year GAAP profitability. QuickLogic continues to rack up impressive partnerships with Honeywell Aerospace, TSMC, and GlobalFoundries, among others. QuickLogic also has contracts with all Top 5 DoD Defense contractors. What separates QuickLogic from other fabless semiconductor companies is their strong belief that FPGA technologies (eFPGA) will be primarily used to support edge AI applications due to their advantages in power consumption and their superior flexibility to support accelerated AI algorithms and software. In addition, it is expected that chiplet architectures will incorporate FPGA into new designs. QuickLogic has a net cash balance sheet, almost 70% gross margins, coupled with strong EPS growth estimates of 94% and 76% in FY24 and FY25, respectively. Quicklogic is expected to generate positive free cash flow in 2025.

Investor Presentation: https://d1io3yog0oux5.cloudfront.net/_a6e2c0e2648510145513f661ad9978f8/quicklogic/db/575/5518/pdf/QuickLogic+IR+Corp+Presentation+Jan+2024+Needham+Final.pdf

Varonis Systems (VRNS)

Varonis is a cybersecurity company with an emerging AI tailwind that is in the process of transitioning to a SaaS model (84% of the company's revenue during the fourth quarter). Varonis provides a comprehensive data security platform to secure critical information, addressing unauthorized access, insider threats, and accidental leaks. Varonis has been racking up important partnerships lately for AI cyber and data security with Snowflake, Microsoft, and Salesforce. In the wake of a surge in generative AI models implementations and development, Varonis’ value proposition is that it protects use of access for AI tools and applications in real time from cyberattacks and also ensures sensitive company data such as passwords, HR records, and intellectual property etc. are safeguarded. The #1 reason CIO’s currently cite for not deploying generative AI models such as CoPilot in their organizations is privacy and security concerns surrounding their data which Varonis can help support. Recently, Varonis announced it had signed a strategic go-to-market partnership with Microsoft to help companies safely implement its new Microsoft Copilot AI software application which should function as a growth tailwind in future years. Varonis estimates call for EPS growth of 72% and 134% in FY25 and FY26, respectively.

Investor Presentation: https://s29.q4cdn.com/507211591/files/doc_presentations/2024/Feb/05/varonis-investor-deck-4q23-vf.pdf

VTEX (VTEX)

VTEX is a Brazilian company that provides enterprises and large retailers with a SaaS e-commerce platform that enables them to more effectively conduct business in Latin America. Latin America is the fastest growing ecommerce growth region which had a CAGR of 29% from 2019-2023. VTEX continues to rack up impressive customer logos and reported $201.5 million revenue for the full year 2023, resulting in a 28% growth in U.S. dollars and 24% on a FX-neutral basis. VTEX also reached an inflection point in their most recent quarter achieving positive GAAP operating margin and positive free cash flow of $9.5M bolstered by existing customers' (~80% of revenues) gross margin reaching 77%, approximately 400 basis points higher than last year. For the full year 2024, VTEX expects continued GAAP profitability with free cash flow and non-GAAP operating income margins to reach mid-to-high single digits. VTEX consensus estimates call for EPS growth of 151% and 232% in FY25 and FY26, respectively.

Investor Presentation: https://s28.q4cdn.com/761427389/files/doc_financials/2023/q4/4Q23-VTEX-Earnings-PPT-pptx-1.pdf

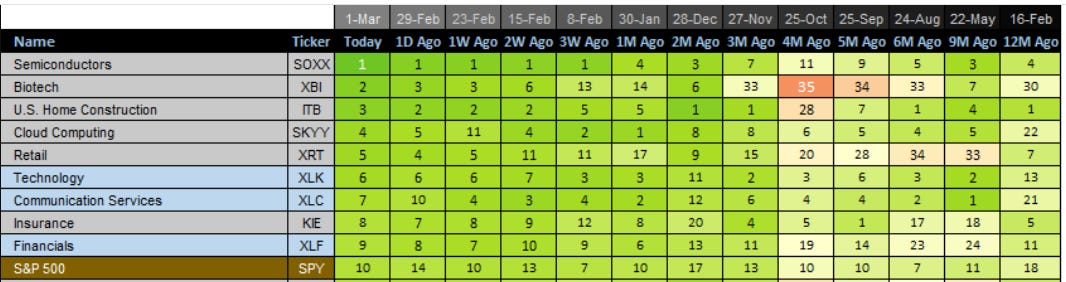

Relative Strength Update

Biotechs (XBI) moved up 11 spots and retail (XRT) up 6 spots over the past 3 weeks. Semiconductors and home construction groups have remained in top 5 market leadership groups over the past 2 months to start 2024.

Quotes of the Week

1) “…We increased our view of the [AI hardware and services] opportunity in the marketplace to $152 billion, 20% CAGR going forward to 2027. And quite frankly, that's probably a lagging indicator. It's still catching up. We think demand continues to be ahead of that. Primarily driven is the overall desire, demand for the computational components to do AI exceeds the supply picture. And quite frankly, it's refreshing to see. We have a high growth category here. That growth is happening certainly in the public cloud, but increasingly more so in enterprises, which is what certainly given our reach in the vast capabilities that we have in business to help customers adopt AI into their business flows, I think it's a big opportunity for us. It's where the data is. 83% of all data is on-prem. We think AI moves to the data. More data will be created outside of the data center going forward than inside the data center today. That's going to happen at the edge of the network. A smart factory, an oil derrick or platform, a deep up mine, all variations of this. We believe AI will ultimately get deployed next to where the data is created driven by latency. And we think about this, the opportunity is to get the training and fine tuning, which is well underway now. But I mentioned earlier this notion about AI in production, inferencing, running the actual tool in production to get the outcomes that businesses want. ……Our enterprise customer base growing, we've sold to education customers, manufacturing customers, governments. We've sold to financial services, business, engineering and consumer services companies. They're seeing vast deployments, proving out the technology. And some cases are using the tooling of the public cloud. And then they quickly find that they want to run AI on-prem because they want to control their data. They want to secure their data. It's their IP and they want to run domain specific and process specific models to get the outcomes they're looking for.”

-Jeff Clarke, Chief Operating Officer, Dell Technologies (DELL)

2) “You go to high tech manufacturing, life sciences and you really got to look at this box and draw a little loop down to reshoring and near shoring. We learned in COVID that supply chains weren't as resilient as they should be. I don't think we learned that, we probably knew that. But we needed to have a lesson like that. So we're seeing our customers move their supply chains back onshore. This was happening even before COVID, because the wage differential versus the transportation and the uncertainty of transportation was not what it was, and automation allow you to make up for a lot of that wage differential….And you go to pharma, biotech, life sciences, again, there's two things happening there. There's reshoring and we're in a lot of the right markets to make that happen, whether it's the Carolinas, parts of California, Indiana or New Jersey. But there's also an explosion of new drugs, specifically around weight loss. And new lines are being added, new capacity, and we're part of that. Then you move to the right, and again, part of that high tech manufacturing is driven by AI and data center buildout….big companies like EMCOR is putting more and more things in the cloud, but also the proliferation of AI, and that needs more systems. These went from 5, 10, 15-megawatt facilities to 50, 80, 100 megawatt facility. So just put that in perspective, if you look at an office building or even a hospital complex, you look at a large hospital complex, that maybe is 5 to 10 megawatts. So think about what that one data center is using today to drive the things we need to be more productive or to outsource or get things into the cloud. Increased power requirements, then you're going to go back to the remodel of some of the data centers that were built to uplift the power in there and also have different kinds of server racks.”

-Tony Guzzi, President and CEO, EMCOR Group (EME)

3) “The market came into 2023 expecting a recession. The market went into 2024 expecting six (6) Fed [interest rate] cuts. The reality is that the U.S. economy is simply not slowing down, and the Fed pivot has provided a strong tailwind to growth since December. As a result, the Fed will not cut rates this year and rates are going to stay higher for longer…..The bottom line is that the Fed will spend most of 2024 fighting inflation. As a result, yield levels in fixed income will stay high.”

-Torsten Slok, Chief Economist, Apollo Global Management (APO)

Some interesting charts from this past week:

1) New Car Inventory- February Update

According to Cox Automotive, US nationwide new car inventories are approaching their highest levels since June 2020 at 80 days of supply. Toyota and Honda continue to have the lowest new car supply while Lincoln, Chrysler, and Dodge have at least twice the industry average at the moment. The slowest selling new cars include the Dodge Hornet (480 days of supply), the Dodge Charger (477 days of supply), and the Ford Mustang Mach-E (362 days of supply). Currently, six of the ten slowest selling cars are Stellantis models.

2) “Magnificent 7” 2023-2025 CAGR Sales Growth Estimates

According to Goldman Sachs Investment Research, the “Magnificent 7” currently comprise 29% of the S&P 500 index and 22% of EPS. Consensus forward revenue growth estimates call for the “Magnificent 7” to grow sales at 4x the rate of the remaining 493 S&P 500 companies through 2025, led by outsized growth from semiconductor and AI leader, NVIDIA. The forward P/E multiple for the Magnificent 7 group stands at 30x vs. 18x multiple for remaining 493 stocks.

3) ApartmentList- Rent Inflation February Update

The Apartment List National Rent Index has proven to be a strong leading indicator of the CPI housing and rent components, since this index captures price changes in new leases, which are only later reflected in price changes across all leases (i.e., what the CPI measures). According to Apartment List National Rent Index, rents were up 0.2% month-over-month but down 1.0% year-over-year in February. This snapped a streak of six consecutive months of rent declines. Today the nationwide median rent stands at $1,377. Overall, 57 of the 100 largest US cities saw rents go up in February, however on a year-over-year basis, rent growth is positive for only 43 of these cities. Many of the steepest year-over-year declines remain concentrated in Sun Belt cities that are rapidly expanding their multifamily inventory, such as Austin (-6.7% year-over-year), Atlanta (-5.3%), and Nashville (-5.1%).

Stocks I’m Watching

Honorable mentions that didn’t make the final cut: DSP, IRON, NXPI, RDNT, ERJ, ARCB, LNW, MRVL, COF, RRR, OTIS, ACVA, JBHT, XEG.TO, PXE, DDS, SKT, UFPI, MANH, SANM, WWD, TALK, STX, HCA, CMPR, GWW, CVLT, PKW, MNDY, APP, CRS, SQSP, ICLR, SNOW, TXT, ATI, FLS, PNR, IMO, TMO, GES, AZO, TSCO, PIPR, RGTI, DCI, ATKR, DY, CXW, SQSP, LPX, MBIN, AVDX, AVPT, KFY, AER, AOS, EOLS, IDXX, PIPR, CARR, FTI, RDNT, TDW, INSW, NET, PLUS, METC, AIT, STLD, PSTG, CLBT, JEF, OWL, EGLE, SBLK, MTDR, CNQ

1) Leonardo DRS (DRS)

Leonardo DRS, Inc., together with its subsidiaries, provides defense electronic products and systems, and military support services.

Leonardo had a strong earnings report last week which was highlighted by their seven nuclear submarine contract for orders for their Columbia Class electric power and propulsion system valued at over $3 billion resulting in a backlog increase of 82% to a record $7.8 billion. Leonardo has become an integral US Navy supplier providing key components of the primary propulsion system of the next-generation ballistic missile submarine fleets and announced it is building a $120M US Navy manufacturing and test facility in Charleston, SC. Consensus forward EPS growth estimates call for Leonardo to grow 22% in both FY25 and FY26 while trading a forward P/E of 19X. Leonardo DRS management will host its investor day on March 14. From a technical perspective, Leonardo broke out of a weekly bull flag is looking for a continuation move higher.

2) NetApp (NTAP)

NetApp, Inc. provides cloud-led and data-centric services to manage and share data on-premises, and private and public clouds worldwide. It operates in two segments, Hybrid Cloud and Public Could.

Data storage names such as NetApp have seen a surge in recent buying as generative AI training and models are shifting to higher performance flash storage vendors and customers are seeking scalable unified data storage systems to capture, aggregate and prepare their internal data for AI application use cases. NetApp posted a beat and raise quarter with NetApp’s flash business growing 21% year-over-year, reaching an annualized revenue run rate of $3.4 billion while it talked up recent contract NVIDIA pod contract wins and helping customers operationalize generative AI workflow models into production environments. NetApp is currently trading at a forward P/E of 12X and has a net cash balance sheet with $500 million of cash. From a technical perspective, NetApp had a weekly base breakout on high volume last week and could off entry opportunity as key moving averages play catch up to Friday’s post earnings gap up. Industry peer Pure Storage (PSTG) also has an almost identical chart and strong post earnings gap up reaction.

3) Micron Technology (MU)

Micron Technology, Inc. designs, develops, manufactures, and sells memory and storage products worldwide.

Micron is approaching an almost 24 year weekly base breakout resistance level at the $96/$97 price level and appears to have two megatrends growth trends supporting its rise at the moment. First, an infant PC replacement cycle with AI functionality coupled with Microsoft’s announcement to retire Windows 10 on October 14, 2025 and the end of support for Windows 11 on November 11, 2025. Second, high bandwidth memory or "HBM" demand which is required for AI chipset uses which should provide expanded profit margins when compared to more basic memory chips. Micron business is highly cyclical but it has become more clear in earnings calls from Dell, Super Micro, Nvidia, among others, that significant capex amounts for memory and storage products will be needed to power generative AI applications. Micron’s earnings estimates reflect a powerful second half of 2024 and 2025 with EPS growth of 92% and 1,855%, respectively.From a technical perspective, Micron is currently extended from its 10WK moving average but could off an entry opportunity on a pullback if it build out a handle on the right side of its weekly base. With a deluge of semiconductor conferences and events taking place in March, news of expanded or new AI partnerships with names such Nvidia, AMD, Dell or a strong earnings report could lead to a powerful base breakout. Earnings are expected 3/20.

Disclaimer:

All investment strategies and investments involve risk of loss. Nothing contained in this website should be construed as investment advice. Any reference to an investment's past or potential performance is not, and should not be construed as, a recommendation or as a guarantee of any specific outcome or profit.