Weekly Stock Bullfinder - Week of 4/15

Weekly Stock Bullfinder - Week of 4/15

Stocks I'm Watching - Week of 4/15

Hope everyone had a nice weekend!

The Not So Good- Commodities Reignite

“I think the 2% [inflation target] is a hard number. We [the United States] have restructured how we frame our economic policy. We have a trillion dollars of fiscal stimulus between the Chips Act, Infrastructure Act, the Inflation Reduction Act (IRA). We have very poor legal immigration policies which is inflationary and restrict jobs…. Inflation has moderated and we’ve always said inflation is going to moderate. But is it going to moderate to that terminal rate the Federal Reserve is looking for? I feel doubtful. Do I believe that we could get a stable inflation between 2.8% and 3%? I’d call it a day and a win.”

-Larry Fink, CEO Blackrock (BLK) April 12th

As the first quarter earnings season begins, we have already seen some nasty market reactions to initial earnings reports from industrial bellwether Fastenal (FAST), JP Morgan Chase (JPM), among others, which have had strong runs so far in 2024. While we were long overdue for a pullback (if the year ended today, the S&P 500's maximum drawdown of -2.49% would still be the smallest of any year in history), post March 1 has seen new market dynamics spring up as more and more inflation prints suggest that further progress on the inflation front has stalled. The Federal Reserve has been telling us that their next move is going to be a cut even though we see solid economic growth and stubborn inflation. As noted in the headline quote, now more and more business media members are attempting to “explain away” why a path back down towards 2% inflation may be wishful thinking and we should “accept it and move on.” Is 3% now the new 2%? In 2023, used car and rental car prices were “explained away” in hot inflation prints and now recently in 2024, car insurance price increases appear to be the topic du jour. In addition, the flow through of recent rises in commodities are bound to show up on upcoming inflation prints.

Since March 1, the commodity complex has woken up and taken on a new life while showing potential signs of emerging into a fresh Stage 2 market uptrend. Base metals including gold, silver, and copper have all joined the rise in energy prices. Believe it or not, XLE is the best YTD performing sector ETF through last week. This comes as China’s economy, a rabid consumer of commodities, is showing signs of stabilization as its March PMI blew through estimates (back in expansion and highest in year) and the gauge for new export orders is also at about one-year highs. In addition, on Friday, the US Treasury announced new sanctions barring import of Russia-origin aluminum, copper and nickel into the US and they have been de-listed from the London Metal Exchange.

The United States Commodity Index Fund (USCI) is comprised of 14 selected contracts which equally weighted and represent five sectors: petroleum (e.g., crude oil, heating oil, etc.), precious metals (e.g., gold, silver, platinum), industrial metals (e.g., zinc, nickel, aluminum, copper, etc.), grains (e.g., wheat, corn, soybeans, etc.), and non-primary sector (e.g., sugar, cotton, coffee, cocoa, natural gas, live cattle, lean hogs, feeder cattle). Last week, the USCI followed through on its weekly breakout as key moving averages look to play catch up to the recent uptrend.

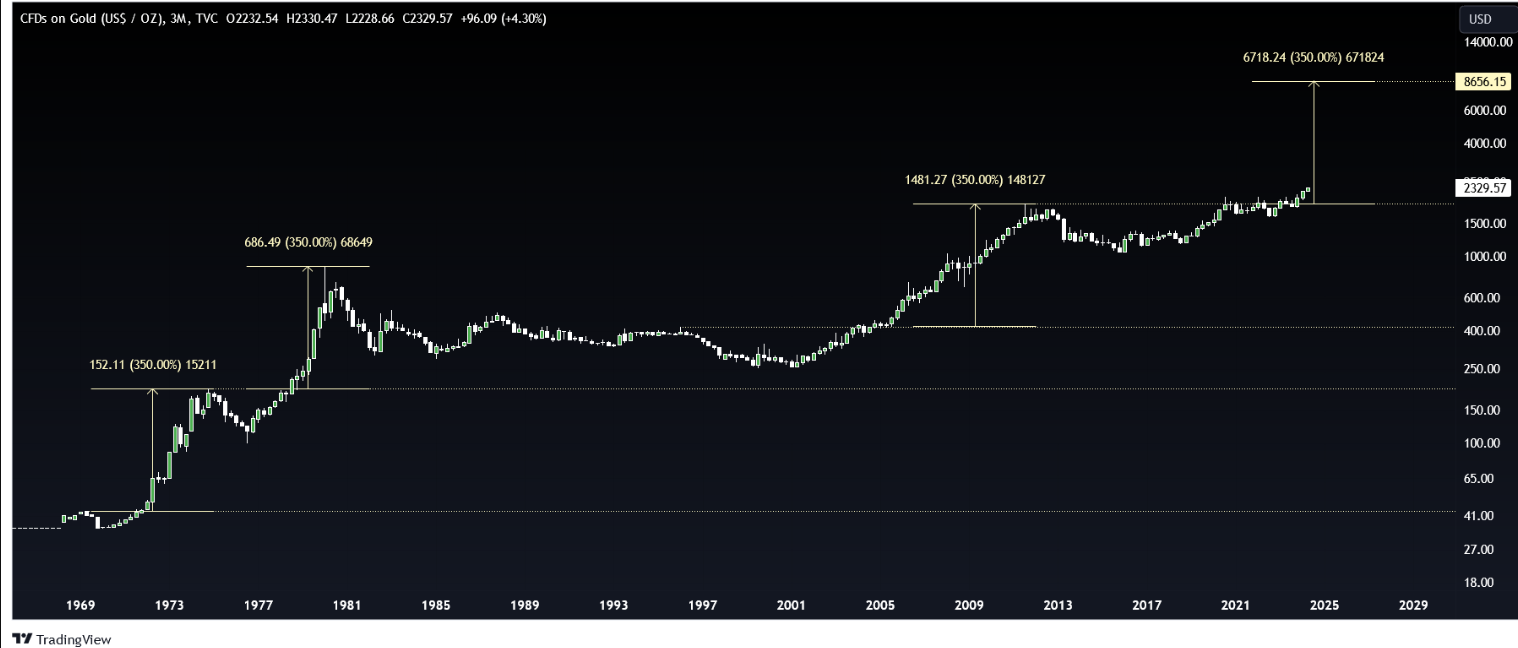

Most notably, the price action in gold has garnered significant attention as central bank purchasing shows no signs of stopping at the moment. Currently, there exists a structural trend towards more gold purchases driven by runaway fiscal deficit spending combined with the major geopolitical fractures that we have in the world today between the U.S. and Europe on one side, and Russia and China on the other. The new gold price records come even as markets start to price out a potential rate cut in June after the March inflation print came in higher than expected. If the past is a good predictor of the future, the last three times gold broke out from a significant high, there was an impulsive move higher of 350%. That would get us to about the $8,600 price level this time.

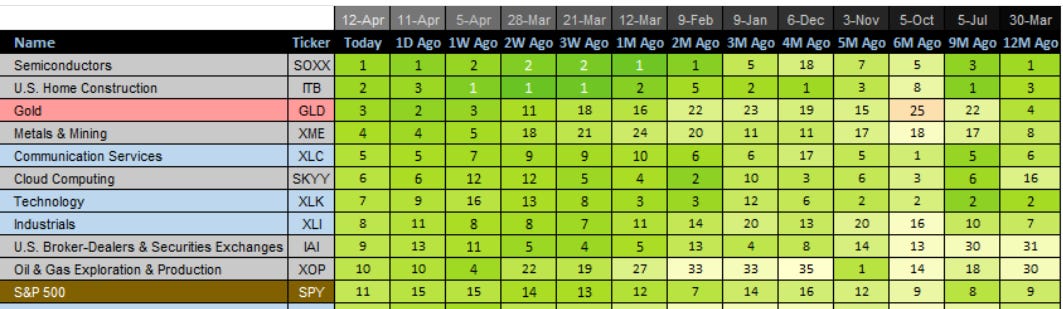

Relative Strength Update

Metals and mining (XME) up 17 spots, gold (GLD) up 15 spots, and oil and gas exploration (XOP) up 9 spots making notable moves the past 3 weeks. Semiconductors (SMH) and home construction (ITB) continue holding up as top relative strength groups.

Quotes of the Week

1) “So, I would say consumer customers are fine. The unemployment is very low. Home prices are up, stock prices are up. The amount of income they need to service their debt is still kind of low. But the extra money of the lower income folks is running out -- not running out, but normalizing. And you see credit normalizing a little bit. And of course, higher-income folks still have more money. They're still spending it. So whatever happens, the customer is in pretty good shape. And if you go to a recession, they're in pretty good shape. Businesses are in good shape. If you look at it today, their confidence is up, their order books are up, their profits are up. But I caution people, these are all the same results of a lot of fiscal spending, a lot of QE, et cetera. And so, we don't really know what's going to happen. And I also want to look at the year. Look at two years or three years, all the geopolitical effects and oil and gas, and how much fiscal spending will actually take place, our elections, et cetera. So, we're in good -- we're okay right now. It does not mean we're okay down the road. And if you look at any inflection point, being okay in the current time is always true. That was true in '72, it was true in any time we've had it. So, I'm just on the more cautious side….And the other thing I want to point out, because all of these questions about interest rates and yield curves and net interest income (NII) and credit losses, it's one thing to project it today based on what -- not what we think in economic scenarios, but the generally accepted economic scenario, which is the generally accepted rate cuts of the Fed. But these numbers have always been wrong. You have to ask the question, what if other things happen, like higher rates with this modest recession, et cetera, then all these numbers change. I just don't think any of us should be surprised if and when that happens. And I just think the chance of happening is higher than other people. I don't know the outcome. We don't want to guess the outcome. I've never seen anyone actually positively predict big inflection points in the economy, literally in my life or in history.”

-Jamie Dimon, CEO, J.P. Morgan Chase (JPM)

2) “Sometimes, people ask us “what’s your next pillar? You have Marketplace, Prime, and AWS, what’s next?” This, of course, is a thought-provoking question. However, a question people never ask, and might be even more interesting is what’s the next set of primitives you’re building that enables breakthrough customer experiences? If you asked me today, I’d lead with Generative AI (“GenAI”)... While we’re building a substantial number of GenAI applications ourselves, the vast majority will ultimately be built by other companies. However, what we’re building in AWS is not just a compelling app or foundation model. These AWS services, at all three layers of the stack, comprise a set of primitives that democratize this next seminal phase of AI, and will empower internal and external builders to transform virtually every customer experience that we know (and invent altogether new ones as well). We’re optimistic that much of this world-changing AI will be built on top of AWS…..Last but certainly not least, Generative AI may be the largest technology transformation since the cloud (which itself, is still in the early stages), and perhaps since the Internet. Unlike the mass modernization of on-premises infrastructure to the cloud, where there’s work required to migrate, this GenAI revolution will be built from the start on top of the cloud. The amount of societal and business benefit from the solutions that will be possible will astound us all.”

-Andy Jassy, CEO, Amazon.com (2023 Shareholder Letter)

3) “For the June quarter, we expect to deliver the highest quarterly revenue in our history of mid-teens operating margin and earnings of $2.20 to $2.50 per share. Our forecast for pre-tax profit of approximately $2 billion is on par with 2019 and just shy of last year, due to higher fuel prices. Demand continues to be strong and we see a record spring and summer travel season with our 11 highest sales days in our history, all occurring this calendar year. Spending on services recently surpassed goods for the first time in five years and there is further runway to return to their long-term trends. Delta's core consumers are in a healthy position and travel remains a top purchase priority. Generational shifts and evolving consumer preferences are driving secular growth in premium experiences. And business travel demand has taken another meaningful step forward this year with growth accelerating into the mid-teens over last year. When you put this level of demand strength together with the industry's increased focus on improving financial returns, this may be the most constructive backdrop that I've seen in my airline career. Our industry-leading performance continues to demonstrate the strength of Delta's differentiated brand and returns-focused strategy. And with our disciplined approach to capital investment and focus on free cash flow, Delta is exceptionally well-positioned to further strengthen our balance sheet and deliver significant shareholder value.”

-Ed Bastian, CEO, Delta Air Lines (DAL)

Some interesting charts from this past week:

1) Average Cost of New U.S. Single Family Home Construction

According to 2022 survey data sourced from the National Association of Homebuilders (NAHB) the average sales price of their single-family homes in 2022 was $644,750 and includes costs for construction, the finished lot, financing, overhead and general expenses, marketing, sales commission, and profit. Total construction costs for the “average” single-family home included in the survey was $392,241. Of the 36 cost subcategories, framing, including the home’s roof, accounts for the biggest chunk at 15.5% of the total construction costs. This is followed by “excavation, foundation, concrete, retaining walls, and backfill” at 10.1%.

2) US CPI Diffusion Index- Under the Hood

In March, the Consumer Price Index (CPI) increased 0.4 percent, seasonally adjusted, and rose 3.5 percent over the last 12 months, not seasonally adjusted. Notably, lagging items such as shelter inflation and car insurance helped contribute to the hot March print. On the other hand, when looking at a diffusion index of the components, the percentage of total CPI items that are below 2% (annualized) has fallen steadily through Q1 (27%) meanwhile the percentage of items >4% (annualized) continues to rise (66%).

3) Indeed Wage Tracker- March 2024 Update- Wage Growth Back to Trend

According to the March update of the Indeed Wage Growth Tracker, posted wage growth in the US has now completed a full round trip and returned to its pre-pandemic pace. Specifically, Indeed’s March data shows annual wage growth of 3.1%, equal to 2019's average. The decline in posted wage growth is broad-based, with 7 in 10 of Indeed’s occupational sectors seeing slower growth in March than in September 2023. Posted wage growth for high and low-wage sectors is now lower in March 2024 than it was in March 2019. The moderation in wage growth aligns with the March BLS employment cost index which showed average hourly earnings increased 4.1% Y/Y last month, the slowest annual increase since June 2021.

Stocks I’m Watching

Honorable mentions that didn’t make the final cut: AXON, NTAP, PSTG, CXT, HSBC, FROG, DSP, CJ.TO, NXE, CVI, OXY, PLAY, ASC, ESEA, HUBS, UEC, OII, TTE, AA, MTDR, USAC, GNK, DINO, INSW, CRS, TECK, MUR, LYB, PWP, DNN, OLN, VTLE, DBB, DK, CF, ARLP, UAN, MGY, NOG, ARES, AVTR, BTE.TO, AR, RY, WPM, ORCL, AGS, TMDX, HSBC, ASX, CP, PAYX, MCHP

1) AeroVironment (AVAV)

AeroVironment, Inc. designs, develops, produces, delivers, and supports a portfolio of robotic systems and related services for government agencies and businesses in the United States and internationally.

DoD funding priorities continue to point to heavy investments in drone and aerial warfare which is AeroVironment’s specialty. Last quarter, AeroVironment reported revenue growth of 38% from a year earlier to $186.6 million and backlog was up 12% from the same quarter last year. Most notably, AeroVironment disclosed that they were in “active negotiations”with the U.S. government on a large multiyear sole-source IDIQ contract for its Switchblade unmanned drones to meet increased demand for the U.S. and its allies. Free cash flow estimates call for surging free cash flow in the years ahead with growth of 451%, 156%, 88%, in 2024-2026, respectively. From a technical perspective, AeroVironment gapped up 18% on huge weekly volume from its weekly base after its most recent earnings report and now key moving averages are playing catch up offering a potential entry opportunity moving forward. Ukraine spending bills or continued geopolitical jitters could also function as a catalyst.

2) Alliance Resource Partners (ARLP)

Alliance Resource Partners, L.P., a diversified natural resource company, produces and markets coal primarily to utilities and industrial users in the United States.

Alliance Resource is primarily a coal company, with roughly $2 billion per year in coal sales, and more than 600 million tons of reserves across the United States. Alliance entered 2024 with over 90% of their coal sales volumes committed and priced at similar levels relative to 2023 allowing for predictability to maintain their higher distribution yields (currently sitting at 13.3% NTM dividend yield). In March, China and India increased their imports of seaborne thermal coal to three-month highs in March as the world's two biggest buyers took advantage of lower international prices of the fuel to meet strong domestic power demand. Recently, Alliance has begun to diversify their royalty segment, by growing their oil and gas royalties business (which delivered record volumes in 2023 and is hedge free to commodity price fluctuations) by acquiring $111 million in additional oil and gas minerals, primarily concentrated in the Permian Basin. From a technical perspective, Alliance found buying interest along its rising 40WK moving average, had a fresh weekly MACD cross, and is showing signs of wanting to move higher.

3) Invesco DB US Dollar Index Bullish Fund (UUP)

The Invesco DB US Dollar Index Bullish Fund is an exchange traded fund which invests in the currency markets by using derivatives and takes long positions in ICE U.S. Dollar Index futures contract to track the value of the US Dollar relative to the Euro, Japanese Yen, British Pound, Canadian Dollar, Swedish Krona and Swiss Franc

The US Dollar Index had a weekly breakout last week as the rapid re-pricing of long term rates and unwind of dovish Federal Reserve interest rate cuts have played out. Fed officials such as dovish members Austin Goolsbee and Mary Daly reiterated they were in “no rush” to cut interest rates and admitted that policy was “appropriate” in light of continued strong employment reports and recent inflation prints which are suggesting that further disinflation progress back down towards the Federal Reserve’s 2% inflation target has stalled in 2024. The markets repricing of the the US dollar and long term interest rates appears to suggest that any near term dovish Fed “pivot” to a cutting interest rate cycle is very murky at best while inflation remains firmly well above its 2% target. In the meantime, there are hints from the Canada Central Bank and ECB that they may cut interest rates in advance of the US Federal Reserve.

Disclaimer:

All investment strategies and investments involve risk of loss. Nothing contained in this website should be construed as investment advice. Any reference to an investment's past or potential performance is not, and should not be construed as, a recommendation or as a guarantee of any specific outcome or profit.