Weekly Stock Bullfinder - Week of 4/22

Weekly Stock Bullfinder - Week of 4/22

Stocks I'm Watching - Week of 4/22

Hope everyone had a nice weekend!

Pullback Afoot Into Earnings Season

With a long overdue market correction afoot, the semiconductor sector finally succumbed to high volume selling and profit taking as ASML Holding, Taiwan Semiconductor, and a lack of a earnings pre-release from AI darling Super Micro Computer (SMCI) spooked investors. Notable declines were seen on Friday with semiconductor names such as Arm (down almost 17%) and Nvidia (down 10%) taking a beating. Profit taking has been taking place across technology groups including long duration stocks which have all suffered due to a surging 10yr yield and stronger dollar.

The AI market thematic which has supported both select technology hardware, semiconductor, software, and industrial data center exposed names will receive a “fresh look” in the upcoming weeks ahead as hyperscaler capex investments come into focus during earnings calls. Expect questions from analysts to scrutinize any changes to capex spending plans, enterprise spending adoption of AI software and tools, and development projects to implement custom chips to diversify reliance solely upon AI leader Nvidia. As shown below, any “wobbles” in capex spending intentions or enterprise demand during this AI investment phase could precipitate continued selling from semiconductor names which have already seen very strong runs over the past 6 months. Analyst could question whether the investment phase of all this capex spending for AI chips, data centers, etc. is ahead of actual market demand or at the level of maturity to achieve near term robust returns on investment spending.

The weekly Bullish Percent Index ($BPSPX) gauges market breadth by tracking the percentage (%) of stocks generating weekly Point and Figure Buy signals. When this gauge exceeds 70%, it suggests an overbought market, & a reading below 35% indicates oversold conditions. As you can see below, this metric began to exhibit a negative divergence in early 2024 and is still appears to have some ways to go before getting firmly into oversold territory where bounces typically occur. Earnings season now arrives with indexes firmly below their 10WK moving average and select stocks (NFLX, FAST, JBHT, etc.) seeing painful post earnings reactions so far to their earnings results. Important to be mindful of cushions heading into earnings season which could be quite bumpy if the current trend continues.

As of Friday’s close, there were only three (3) S&P 500 sectors that still have at least 50% of constituents above their respective 100 day MAs: Energy: 68% Industrials: 53%, and Materials: 57%. Could this be signaling that the economy still remains strong but is now re-adjusting to a higher for longer interest rate environment?

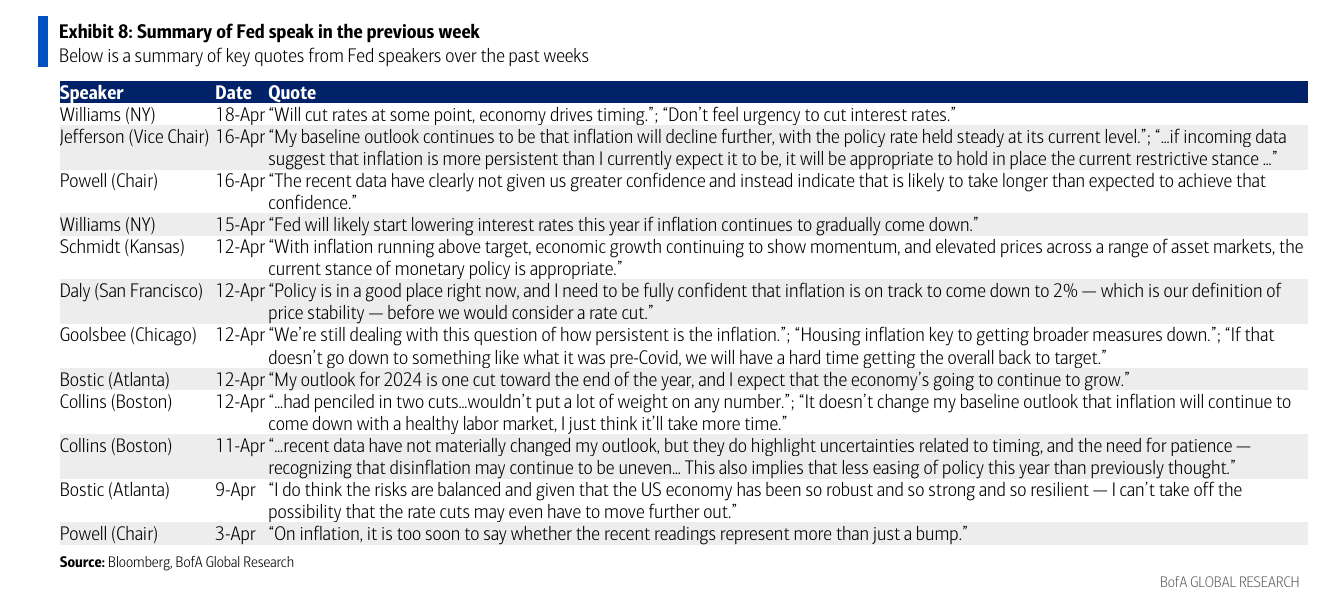

With the Federal Reserve officials entering a blackout period this week (April 20- May 2) and the March PCE reading, the Fed’s preferred inflation metric, set to be released this Thursday, the chorus of “FedSpeak” comments continue to suggest a pushback against market expectations for an interest rate cutting cycle to begin in 2024. Almost all Fed officials, including “dovish” Fed officials, frequently describe the current progress on lowering inflation as “stalling”.

Relative Strength Update

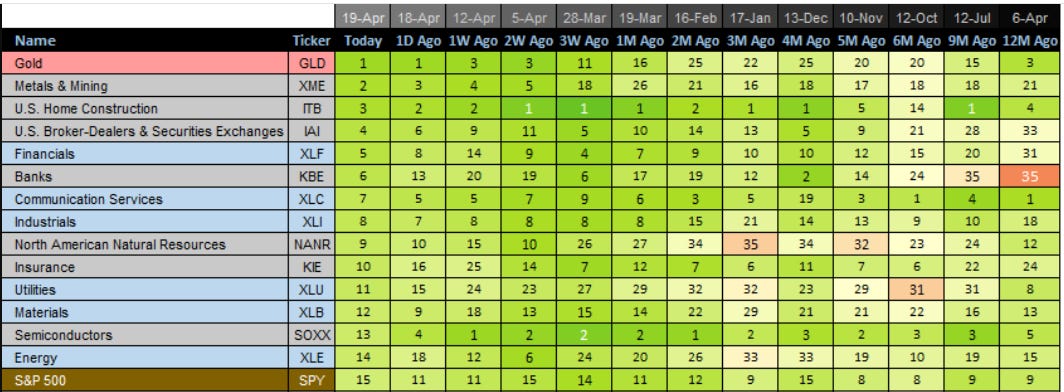

This weeks relative strength update provides evidence of a market rotation and correction afoot with gold (GLD) now taking the top relative strength spot. The biggest relative strength increases over the past 3 weeks have also come from metals and mining (XME, + 16 spots), natural resources (NANR, +17 spots), and utilities (XLU, +16 spots).

Quotes of the Week

1) “Well, there are going to be different [artificial intelligence] bottlenecks. Over the last few years, I think there was this issue of GPU production. Even companies that had the money to pay for the GPUs couldn't necessarily get as many as they wanted because there were all these supply constraints. Now I think that's sort of getting less. So you're seeing a bunch of companies thinking now about investing a lot of money in building out these things. I think that that will go on for some period of time. There is a capital question. At what point does it stop being worth it to put the capital in? I actually think before we hit that, you're going to run into energy constraints. I don't think anyone's built a gigawatt single training cluster yet. You run into these things that just end up being slower in the [real] world. Getting energy permitted is a very heavily regulated government function. You're going from software, which is somewhat regulated and I'd argue it’s more regulated than a lot of people in the tech community feel…. We interact with different governments and regulators and we have lots of rules that we need to follow and make sure we do a good job with around the world. But I think that there's no doubt about energy. If you're talking about building large new power plants or large build-outs and then building transmission lines that cross other private or public land, that’s just a heavily regulated thing. You're talking about many years of lead time. If we wanted to stand up some massive facility, powering that is a very long-term project. I think people do it but I don't think this is something that can be quite as magical as just getting to a level of AI, getting a bunch of capital and putting it in, and then all of a sudden the models are just going to… You do hit different bottlenecks along the way.”

-Mark Zuckerberg, CEO Meta Platforms (META)

2) “Looking at the full year 2024, macroeconomic and geopolitical uncertainty persists, potentially further weighing on consumer sentiment and end-market demand. We thus expect the overall semiconductor market, excluding memory, to experience a more mild and gradual recovery in 2024. We lowered our forecast for the 2024 overall semiconductor market, excluding memory, to increase by approximately 10% year-over-year, while foundry industry growth is now forecast to be mid- to high-teens percent, both are coming off the steep inventory correction and/or base of 2023…The continued surge in AI-related demand supports our already strong conviction that structural demand for energy-efficient computing is accelerating in an intelligent and connected world. TSMC is a key enabler of AI applications. Almost all the AI innovators are working with TSMC to address the insatiable AI-related demand for energy-efficient computing power. We forecast the revenue contribution from several AI processors to more than double this year and account for low-teens percent of our total revenue in 2024. For the next 5 years, we forecast it [AI] to grow at 50% CAGR and increase to higher than 20% of our revenue by 2028. Several AI processors are narrowly defined as GPUs, AI accelerators and CPU's performing, training and inference functions and do not include the networking edge or on-device AI. We expect several AI processors to be the strongest driver of our HPC platform growth and the largest contributor in terms of our overall incremental revenue growth in the next several years.”

-C. C. Wei, Taiwan Semiconductor Manufacturing Co Ltd (TSM)

3) “The firm's thematic approach to deployment is informed by the real time data and insights we gather from our global portfolio, which helps us to identify trends early and build conviction around our ideas…..We identified QTS, the fifth largest US data center REIT as a well positioned but poorly trading public company with tremendous long term potential. Our BREIT, BIP Infrastructure and BPP perpetual strategies acquired the company for $10 billion in 2021, and its lease capacity has already grown sixfold in less than three years. Today, QTS is the largest data center company in North America. We are building a variety of other center platforms around the world as well. In total, Blackstone vehicles now own $50 billion of data centers globally, including facilities under construction. And there is an additional $50 billion in prospective future development pipeline….There are several other powerful megatrends that we expect to drive the firm forward, both in terms of where we invest and where we raise capital. The most compelling of these today include the secular rise of private credit, where we have one of the world's largest platforms; infrastructure, energy transition, life sciences and the expansion of alternatives globally and particularly in Asia…Looking forward in 2024, the market environment will remain complex. The economy is stronger than expected but is starting to slow a bit. In terms of inflation, despite the recent US CPI readings, we are seeing a decelerating wage growth and minimal input cost increases across many of our companies. In real estate, we see shelter costs moderating, contrary to government data. We believe inflation will trend lower this year, although, the pace of decline has slowed recently.”

-Steve Schwarzman, CEO Blackstone Inc. (BX)

Some interesting charts from this past week:

1) Manheim Used Car Index- Mid April Update

Through mid-April, the Manheim Used Car Value Index continues to pullback and has now fallen by 22.7% from its all-time high. The mid-month Manheim Used Vehicle Value Index dropped to 199.2, which was 13.7% lower than the full month of April 2023. Electric vehicles (EVs) were down 18.3% against values for April 2023, while non-EVs declined by 13.1% over the same period. The current pullback represents by far the worst drawdown in the index's history, however prices are still hovering 25-30% above pre-pandemic levels.

2) Multifamily Apartment Completion Estimate

Yardi Matrix updated their multifamily unit forecast including their predictions for new apartment completions in more than 100 U.S. markets from 2024-2029. Yardi Matrix research supports there will be a sizable under construction pipeline coming to completion in 2024 and 2025 with supply bottoming in 2026. New unit completions will peak this year with 550,000 units coming to the apartment market. Austin leads U.S. markets in the most apartment units headed to market, with 98,842 units expected to be completed through 2029. Phoenix (91,852) is next, followed by Denver (76,846), Charlotte (74,791), North Dallas (70,146), West Houston (69,417), Orlando (65,476), Nashville (59,504), and Miami (58,658).

3) 1Q24 FactSet Estimates S&P 500 Earnings Growth

With Microsoft, Meta Platforms, and Alphabet scheduled to report earnings results this week (in total 42% of the S&P 500 index reports this upcoming week), its noteworthy that five of the seven companies in the “Magnificent 7” are projected to be the top five contributors to year over-year earnings growth for the S&P 500 for Q1 2024. These five companies (in order of highest to lowest contribution) are NVIDIA, Amazon.com, Meta Platforms, Alphabet, and Microsoft. The “Magnificent 7” companies in total are expected to report year-over-year earnings growth of 64.3% for the first quarter. Excluding these five companies, the blended (combines actual and estimated results) earnings decline for the remaining 495 companies in the S&P 500 would be -6.0% for Q1 2024. Wall St. analysts predict these five companies in aggregate will report year-over-year earnings growth of more than 15% for the remaining three quarters of 2024.

Stocks I’m Watching

Honorable mentions that didn’t make the final cut: RJF, LPLA, HTGC, WFC, JBI, CXT, ARLP, HCC, ISRG, GS, CLBT, ARES, DELL, AVAV, STNG, ASC, MUR, DVN, VKTX

1) Elevance Health (ELV)

Elevance Health, Inc., together with its subsidiaries, operates as a health benefits company in the United States. The company operates through four segments: Health Benefits, CarelonRx, Carelon Services, and Corporate & Other.

Both Elevance Health and UnitedHealth reported earnings last week that impressed Wall St. as both health insurers exceed Wall Street expectations as their medical care ratios, the portion of premiums spent on healthcare costs, improved from the prior quarter and premium rate adjustments implemented helped to cover medical cost trends. Elevance also raised its full-year outlook for adjusted diluted EPS to above $37.20, compared to $37.15 in the consensus and above $37.10 in its prior forecast. EPS estimates call for growth of 37%, 14%, and 12% from 2024-2026, respectively. From a technical perspective, Elevance its $533 weekly breakout resistance level and could follow through in coming weeks if defensive market positioning continues.

2) Raytheon Technologies (RTX)

RTX Corporation, an aerospace and defense company, provides systems and services for the commercial, military, and government customers in the United States and internationally.

Raytheon was punished during 2023 for the one-time Geared Turbofan engine recall impact (>$20B market cap vs ~$3B cost), and analysts expect sentiment should improve as the grounded aircraft backlog peaks and starts to move lower. Continued geopolitical developments have again brough companies back to devoting additional spending budgets to restocking and increasing defense supplies. Finishing 2023, Raytheon’s backlog swelled to a record $196 billion with 60% of the backlog on its defense side set to liquidate over the next 2 years. In addition, Raytheon has guided to a strong year as free cash flow is expected to grow from $5.5 billion to $5.7 billion for 2024 and to $7.5 billion in 2025. Raytheon also has a strong buyback program in place which has served to reduced shares outstanding by almost 10% in 2023. Earnings estimates call for EPS growth of 90%, 17%, and 13%, from 2024-2026, respectively. From a technical perspective, Raytheon is consolidating into a weekly bull flag as key moving averages play catch up heading its earnings report this week. Earnings expected 4/23. A strong report and passage of additional Ukraine funding could lead to a continuation breakout.

Disclaimer:

All investment strategies and investments involve risk of loss. Nothing contained in this website should be construed as investment advice. Any reference to an investment's past or potential performance is not, and should not be construed as, a recommendation or as a guarantee of any specific outcome or profit.