Weekly Stock Bullfinder - Week of 8/15

Weekly Stock Bullfinder - Week of 8/15

Stocks I'm Watching - Week of 8/15

I hope everyone had a nice weekend!

All Things Clean Energy Rally- Can It Last?

The last month and a half has featured a significant character change in all things clean energy whose timing came alongside the announcement of the US government’s largest fiscal spending package for renewable energy investment. We are now potentially witnessing the first “follow through” effect of the Russia/Ukraine conflict which is that nations are waking up to the fact that energy security and infrastructure must be given a much higher priority and investment must be made to grow sources of supply in order to have stable and lasting economic growth. This secular trend is still in its very early innings from an investment standpoint. For example, according to the July IEA report on global EV supply chains (https://www.iea.org/reports/global-supply-chains-of-ev-batteries), there is a global need for 50 more lithium mines, 60 more nickel mines, and 17 more cobalt mines by 2030 to meet country announced emission pledges scenario. Per Brookfield Asset Management’s 2Q shareholder letter:

“Energy Transition- Trillions of dollars will be required by 2050 for energy transition as energy grids are converted to more renewables, and as the developing markets move off coal and onto natural gas and renewables. In addition, the electrification of industry and transport will require that trillions be invested in electrical battery plants and other infrastructure for decarbonization of high emitting and hard to ebate sectors.

Rewiring of European Energy- Given the recent geopolitical events in Europe, unprecedented capital will be required to rebuild the European backbone infrastructure in order to enable energy self-sufficiency. This will include nuclear, LNG regasification facilities, energy storage, hydrogen and large scale renewables”

In the near term, several significant clean energy ETF’s are now approaching their crucial “make or break” resistance points for closely followed and highly liquid clean energy sector ETF’s like ICLN, TAN, and PBW. The price and volume action at these resistance points could provide clues as to this rally has continued staying power in the upcoming weeks ahead and whether this sector can provide market leadership. Solar names in particular continue to be on fire but may need some time to cool off and let the moving averages catch up.

Some interesting charts from this past week:

1) Consumer Stress Index

Strategas Research put out an update to the consumer stress indicator graph last week that combines the food at home inflation rate, mortgage rate, and gas prices. Last week’s updated showed that the consumer stress indicator remains at 23% for the 2nd straight month despite mortgage rates and gasoline prices falling significantly from June. The CPI release last week showed that the food at home component is now growing at 13% which offset the decline in the other two components. Bottom line, while there is relief in certain pockets of pricing pressures, consumers remain stressed from historical trends and levels.

2) Atlanta Fed Wage Growth Tracker- July Update

The Atlanta Fed released their updated Wage Growth Tracker for the month of July. The Atlanta Fed's Wage Growth Tracker is a measure of the nominal wage growth of individuals. It is constructed using microdata from the Current Population Survey (CPS), and is the median percent change in the hourly wage of individuals observed 12 months apart. Income increases remain fairly widespread and continuing their upward trend.

-Median nominal wages +6.7% YoY

-Median wages for prime-age workers +6.9%

-Median wages for job switchers +8.5% (quits rate = 2.8%)

https://www.atlantafed.org/chcs/wage-growth-tracker

3) Electric Vehicle Battery Manufacturer Market Share

The graph below shows the current market share of EV battery manufacturers in the world. The top 10 battery manufacturers are all headquartered in Asia with Chinese owned CATL holding almost 33% of current market share. CATL is also key battery supplier to Tesla. The top 3 battery manufacturers account for almost 70% of the current market share.

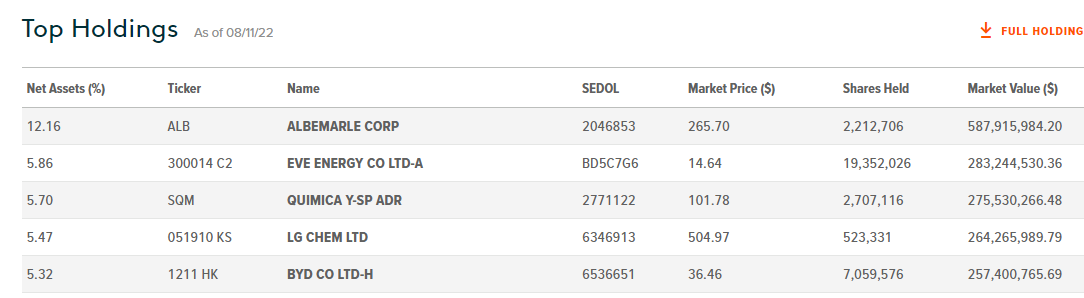

Stocks I’m Watching

1 & 2) Albemarle (ALB) & Global X Lithium ETF (LIT)

Albemarle Corporation develops, manufactures, and markets engineered specialty chemicals worldwide. It operates through three segments: Lithium, Bromine, and Catalysts. The Lithium segment offers lithium compounds, including lithium carbonate, lithium hydroxide, lithium chloride, and lithium specialties; and reagents, such as butyllithium and lithium aluminum hydride for use in lithium batteries for consumer electronics and electric vehicles, high performance greases, thermoplastic elastomers for car tires, rubber soles, plastic bottles, catalysts for chemical reactions, organic synthesis processes in the areas of steroid chemistry and vitamins, life sciences, pharmaceutical industry, and other markets. The Bromine segment offers bromine and bromine-based fire safety solutions; specialty chemicals, including elemental bromine, alkyl and inorganic bromides, brominated powdered activated carbon, and other bromine fine chemicals for use in chemical synthesis, oil and gas well drilling and completion fluids, mercury control, water purification, beef and poultry processing, and other industrial applications; and other specialty chemicals, such as tertiary amines for surfactants, biocides, and disinfectants and sanitizers. The Catalysts segment provides hydroprocessing, isomerization, and akylation catalysts; fluidized catalytic cracking catalysts and additives; and organometallics and curatives.

The recent “Inflation Reduction Act” (IRA) has ignited a significant rally in the clean energy sector as noted above but the EV battery clauses were a under the radar catalyst as well for materials names like lithium producers. The IRA legislation stipulates that makers of electric vehicles must assemble their vehicles in North America and source most of their battery components and materials - including lithium - from countries with trade-friendly agreements in place with the U.S., in effect removing China's significant lithium supply from the equation. There is a gradual phase in of this requirement that increases each year through 2028. This provides a huge tailwind to established lithium producers with North American operations like Albemarle, Livent, and SQM who are already benefiting from skyrocketing lithium prices that have jumped almost 400% year over year. Other beneficiaries include tickers PLL, LAC, and MP. As a result, this will require EV makers to radically re-think their battery supply chains otherwise risking have their EV fleets not eligible for the $7,500 federal tax credit.

Albemarle and Livent have already put up huge earnings reports, and SQM is reporting in the middle of the week which is anticipated to be another very strong report. SQM also holds the 3rd highest weighting in the LIT ETF which is now breaking through its 200 day moving average and may be forming the right side of its base after breaking its downtrend. Albemarle looks to be putting in a double bottom base and could go higher after yet another beat and raise quarter. Last quarter, Albemarle reported that its expects EBITDA will rise by 500%-550% Y/Y and average realized pricing is now expected to increase 225%-250% due to renegotiated contracts and increased market pricing. Due to its blowout results this year, Albemarle has seen significant P/E multiple compression with its forward P/E shrinking from 41X at the very beginning of the year to just 8X as of last Friday’s market close. Investors may be waking up to the significant pricing power these lithium producers will yield going forward as mining delays and now the IRA act further puts supply chain pressures on EV manufacturers.

3) Tata Motors (TTM)

Tata Motors Limited designs, develops, manufactures, and sells various automotive vehicles. The company offers passenger cars; sports utility vehicles; intermediate and light commercial vehicles; small, medium, and heavy commercial vehicles; defense vehicles; pickups, wingers, buses, and trucks; and electric vehicles, as well as related spare parts and accessories. It also manufactures engines for industrial and marine applications; aggregates comprising axles and transmissions for commercial vehicles; and factory automation equipment, as well as provides information technology and vehicle financing services. The company offers its products under the Tata, Daewoo, Harrier, Safari, Fiat, Nexon, Altroz, Punch, Tiago, Tigor, Jaguar, and Land Rover brands. It operates in India, China, the United States, the United Kingdom, rest of Europe, and international.

The global EV market is ramping at an accelerated pace and broadening out to developing countries such as India. One player in particular, Tata Motors owns a commanding 90% market share of EV’s sold in the country and government there has implemented significant barriers to entry to promote domestic production of Indian EV’s. In fact, Tesla recently pulled out of negotiations to enter India earlier this year after failing to come to terms with the government. In the meantime, Tata continues to make significant production growth in its EV business and its CEO recently said that Tata intends to sell about 50,000 electric vehicles by the end of FY ending March 31 and double that in the 2023/24 period. In 2021/22, the company sold 19,105 EVs, +353% Y/Y. Earnings estimates for FY23 are explosive and call for revenue growth of 580% and EBITDA margins growing 4X to 11.2%. While Tata still owns legacy auto brands like Jaguar and Land Rover, I suspect this company over time will start being valued similarly its EV peers as sales mature of the next few years. In early August, Tata announced sales growth of 51% year-over-year for July 202 with EV sales growing 566% YoY. From a technical perspective, Tata is seeing significant accumulation of the right side of its current base and is now attempting to follow through from its 200 day moving average.

Disclaimer:

All investment strategies and investments involve risk of loss. Nothing contained in this website should be construed as investment advice. Any reference to an investment's past or potential performance is not, and should not be construed as, a recommendation or as a guarantee of any specific outcome or profit.